The deployment of carbon capture and storage is crucial to achieve substantial reductions in upstream emissions. CCS has the potential to reduce lifecycle emissions of upstream oil and gas assets by up to 60%, according to Vantage Upstream Enhanced Emissions datasets from S&P Global Commodity Insights. This reduction is contingent upon several factors, including the CO2 content of resources, and the timeline between hydrocarbon production and CCS implementation.

Environmental regulations aimed at reducing emissions from reservoir CO2 venting could also serve as a catalyst for advancing CCS in Asia-Pacific, but there is no unified strategy in the region to address this.

With its reformed Safeguard Mechanism, Australia is the only country in the region which has a policy in place that restricts CO2 venting emissions, establishing a zero-emissions baseline for reservoir CO2 from new gas fields.

The policy requires operators to mitigate reservoir CO2 emissions from new gas fields through CCS or other methods. Failing this, they will be required to offset the emissions by surrendering Australia Carbon Credit Units or Safeguard Mechanism Credits, incurring additional costs to production.

Typical policies could compel operators to shift their focus toward production from fields with lower reservoir CO2 concentrations. However, such regulatory measures could also create tension with national priorities surrounding affordable energy supply. Balancing these interests will be crucial as oil and gas players navigate their path toward net-zero.

Upstream oil and gas CCS outlook

CCS for upstream oil and gas is expected to account for 18% of overall global capture capacity by 2035, according to a Commodity Insights CCUS industry trends report. Capture capacity for upstream oil and gas by 2035 is estimated to reach 70 million mt/year.

Asia-Pacific leads in the construction and advanced phase of development projects, followed by North America and the Middle East.

As the global energy landscape undergoes transformation, Asia-Pacific is at a pivotal point in reconciling energy demand with the imperative of achieving net-zero emissions.

The region’s energy mix remains predominantly reliant on fossil fuels and, during this transitional phase, several countries are estimated to maintain a dependence on hydrocarbon fuels, particularly natural gas.

Asia-Pacific has 5 million mt/year of CCS capacity under construction, while 7 million mt are in advanced stages of project development, according to Commodity Insights’ CCUS projects and hubs database. This capacity is estimated to reach 23 million mt/year by 2035.

Commodity Insights estimates that upstream emissions from CO2 venting in the region without CCS are expected to reach 75 million mt/year by 2035, highlighting the need for additional capacity to reduce emissions from the upstream oil and gas sectors.

Navigating emissions challenges

High CO2 fields have been a major source of hydrocarbon production in Asia-Pacific. Considering the necessity to meet marketable gas specifications, a large portion of the extracted CO2 must be separated from the hydrocarbon gas.

This separation leaves waste gas with a high CO2 concentration being vented into the atmosphere, significantly boosting production emissions levels. This venting becomes the major source of upstream emissions in Asia-Pacific, alongside emissions from other activities such as fuel gas and diesel combustion, flaring, and methane fugitives and venting.

As a result, despite progress made through operating and sanctioned CO2 injection, projections indicate a rise in CO2 venting from upstream assets — particularly from unsanctioned projects at the regional level — if deployed without CCS.

Commodity Insights estimates that CO2 venting intensity from upstream oil and gas in Asia-Pacific could rise seven times higher than 2023 level by 2050.

While other upstream emissions sources, like fuel combustion and flaring, are expected to decrease by about 65% by 2050, the emissions from upstream CO2 venting in Asia-Pacific could increase from an average of 34 million mt/year in recent years to 56 million mt/year by 2035 and 139 million mt/year by 2050.

This projection considers the amount of captured and injected CO2 from CCS projects currently in the pipeline, which capture reservoir CO2 from oil and gas projects that are operating and those expected to operate by the end of this decade.

The increase is largely driven by vented reservoir CO2 from unsanctioned upstream projects, or projects for which a final investment decision has not been taken, which will contribute to 58% of the region’s total production volume but contribute to more than 80% of the Asia-Pacific’s upstream emissions in 2050.

Additionally, about 30% of the region’s total production volume is expected to come from fields with formation CO2 content higher than 10%, compared to about 15% in 2023 .

These assumptions are not based on oil and gas supply forecasts. Instead, they are based on discovered and appraised fields anticipated to come online in the future, driven by their favorable economics. It is important to note that these projections do not include volumes that have yet to be discovered.

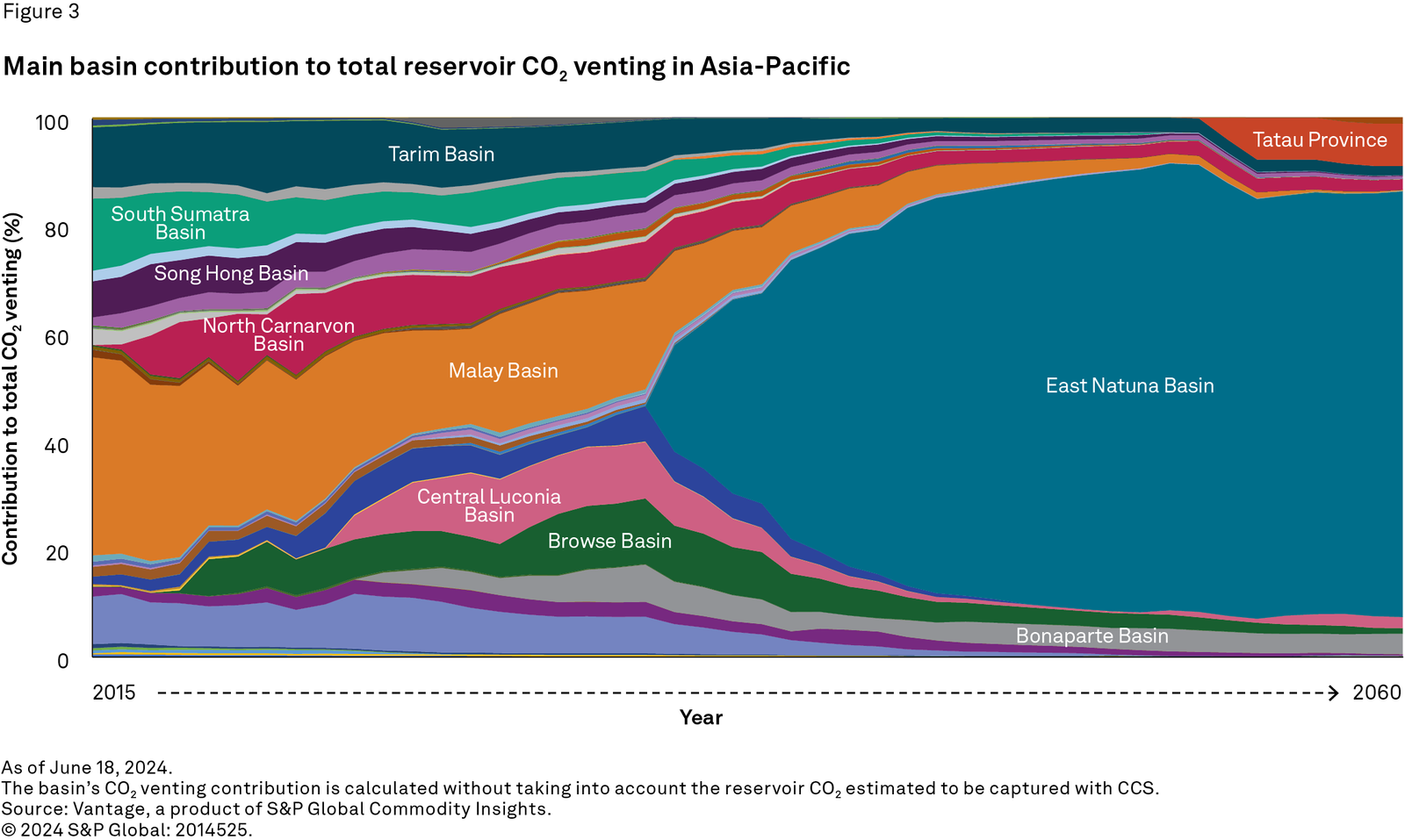

Many of these unsanctioned assets are centrally distributed in key basins, such as the East Natuna and Malay basins that are located in Indonesia, Malaysia, Thailand and Vietnam. This highlights a potential pathway for developing CCS hubs in these basins, which would not only help mitigate reservoir CO2 emissions for the upstream production at lower costs but also offer options to abate CO2 emissions from nearby industrial facilities.

Further reading: