")

J. Michael Jones

Shares of Brixmor Property Group (NYSE:BRX) have been a modest performer over the past year, rising about 8%. Elevated interest rates have weighed on real estate valuations, though shares have seen some momentum recently as expectations around Federal Reserve rat cuts have risen. I last covered BRX in November, rating shares a buy, and since then, they have performed in line with the market, gaining 19%. With BRX just reporting Q2 results and rate cut hopes rising, now is an opportune time to revisit shares. I remain bullish.

Seeking Alpha

In the company’s second quarter, Brixmor generated $0.54 in funds from operations, $0.02 ahead of consensus, as revenue rose by 2% to $316 million. Overall, this was a strong quarter as the company continues to benefit from rising occupancy and strong lease renewal activity. While traditional malls have felt significant pressure, Brixmor operates open-air facilities that have proven much more resilient.

Brixmor’s assets are in demand

About 80% of base rent comes from grocery anchored centers. Grocery stores face less risk from e-commerce trends and help to bring steady daily traffic to centers, which helps drive business for small shops. Additionally, Brixmor’s properties are in fairly desirable areas, including a meaningful Sun Belt presence, and they serve customers with a $105k average household income. Its upper middle-class customer base has proven more resilient to inflationary pressures that have weighed on lower-income consumers.

Additionally, while grocery-anchored centers are a bit of a unique asset class in my view, the general concern around brick and mortar retail has limited new construction. This lack of supply has helped create favorable leasing conditions, which were apparent in Q2 results. In fact, during the quarter, there were 0.6 million square feet of new leases at a 50.2% spread. Including renewables, Brixmor did 1.4 million square feet of leasing at a 27.7% spread. As these new leases commence, Brixmor will see meaningful base rent growth.

Importantly, Brixmor also has quality anchors, especially after releasing Bed Bath and Beyond’s space last year. Its top tenants are large, quality retailers, which limits bankruptcy risk, though we may see Dollar Tree (DLTR) close some locations over time. Additionally, its top ten tenants represent less than 17% of base rent, reducing counterparty risk and speaking to the high level of diversification in its business.

Brixmor

Q2 leasing will drive ongoing revenue growth

Now, as noted earlier, Brixmor saw strong releasing activity in Q2, and this is driving occupancy higher. Total occupancy was at 95.4% (up 30bps sequentially), anchors at 97.5% (up 20bps sequentially), and small shops at 90.8% (up 30bps sequentially), all records. Anchor occupancy runs structurally higher than small shops (anecdotally, at your local grocery center, you have likely noticed the small stores turn over more frequently than the grocery store), but small shops pay higher lease rates.

Thanks to releasing and increased occupancy, same property net operating income rose by 5.5%, aided by 3.8% base rent growth. Same-property lease rates rose 120bps to 95.4% from last year. Importantly, there is also a clear avenue for future growth. New tenants lease space before they begin occupying it. Right now, there is a 400bps leased to billed occupancy gap. That is $65 million of pending base rent from not yet occupied spaces. That is another 5% tailwind to annual revenue as these units flip to paying rent over the next 12-18 months. On top of that, with its strong releasing environment, we should see favorable cash spreads on new leases in coming quarters. This points to ongoing 4-5% revenue growth over the next 24 months in my view.

Increasing occupancy is also supporting wider margins because much of the cost of a center is fixed whether half-full or entirely occupied. Operating costs rose by 3.4%. Property taxes were down $7 million, while interest expense rose by $6 million. As a result, same property margins expanded 200bps to 75.8%, and adjusted EBITDA of $220 million was up by 9%.

Leasing activity continues to exceed my expectations. In fact, alongside results, management was able to raise guidance. For the full year, it expects $2.11-$2.14 FFO from $2.08-$2.11 previously with same property NOI growth up 75bps from its prior range to 4.25-5%. Back in November, I was targeting $2.06-$2.11 of FFO, so guidance now exceeds the top end of my expectations. Importantly, with that 400bp leased-not-occupied backlog, there is a clear avenue for ongoing rental revenue growth. This provides visibility around the next several quarters and gives strong credibility to guidance.

Beyond leasing activity, Brixmor continues to invest moderately in its properties to enhance their attractiveness and boost rents. It has a $510 million investment pipeline at a 9% anticipated yield. In Q2, seven projects totaling $37 million were completed, providing a 9% incremental yield. This is a methodical pace of spending that Brixmor can afford.

Brixmor’s balance sheet and retained cash create resiliency

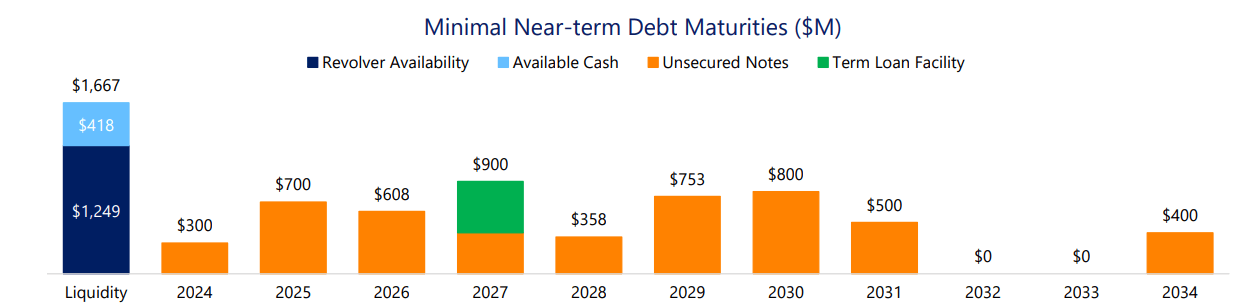

First, it has a solid balance sheet with 5.6x net debt/EBITDA leverage. It has a $5.4 billion debt load, which is well-staggered, as you can see below. It has also issued 2035 debt to handle its 2024 maturity.

Brixmor

Because its debt is well-laddered, I do not view BRX’s financials as having significant interest rate sensitivity. That said, I do view interest rates as an important risk for BRX’s share performance. Interest rates can drive real estate valuation and impact the relative attractiveness of dividend stocks.

If we were to see long-term rates rise again, that will create an alternative for yield-seeking investors and can weigh on REIT valuations. I do not expect a sharp Fed rate cutting cycle; however, I do expect rate cuts to begin in September. If rates are stable to decline, that will enable Brixmor’s underlying growth to push shares higher. If, however, rates rise back above 4.5% on the 10-year treasury, I would expect BRX to underperform the market.

Finally, I would note that BRX is retaining substantial cash flow. BRX will retain at least $305 million in cash after its dividend, which it can use to fund growth projects without needing significant incremental borrowings. This further reduces direct interest rate risk on its business. This strong coverage also means its dividend is secure in my view. In fact, I expect BRX to raise its dividend later this year.

Brixmor can raise its dividend steadily, making shares attractive

Shares have a 4.4% dividend yield. At $0.2725, its dividend is still $0.0125 below pre-COVID levels. With results so strong, I expect a dividend increase later this year, likely to $0.285, bringing it back to pre-COVID levels. That would still leave shares with a robust 1.85x dividend coverage ratio, paving the way for ongoing increases.

Brixmor delivered a strong second quarter, and given supply constraints, we continue to see very favorable leasing dynamics, which should drive revenue growth into 2026. I expect about $2.13 in FFO this year and 4-5% growth off this level in each of the next two years. With its elevated dividend coverage, I expect its dividend payout to rise more quickly than FFO for several years, as a business like this can run at 1.6-1.7x coverage comfortably.

Even after their recent rally, shares have an 8.6% FFO yield, which I view as attractive given its growth prospects. At a 1.65x coverage, its theoretical dividend capacity is ~$1.30, giving shares a potential 5.25% capital return yield. With FFO likely to grow 4-5%, this initial yield is attractive in my view. I see shares moving to at least $26, or a 5% “potential” dividend yield. Combined with its dividend, that is a ~10% total return over the next year.

With its high-quality assets, visible revenue growth, and strong dividend coverage, BRX remains a “buy” for income growth-oriented investors. Barring a surprise rebound higher in interest rates, I expect recent momentum to continue and reiterate BRX as a buy after strong Q2 results.