DKosig

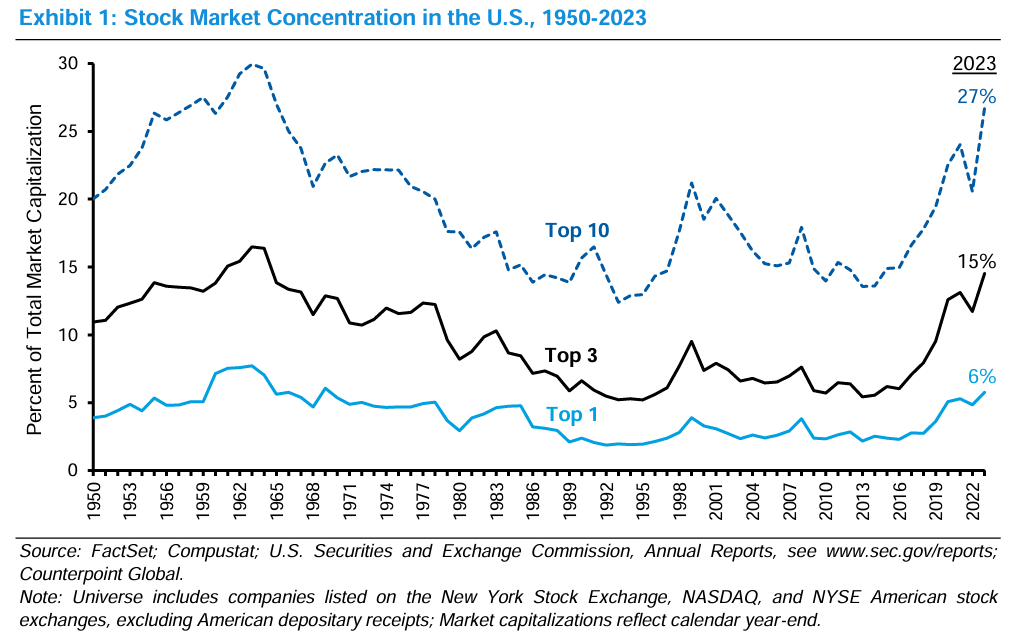

U.S. equities have enjoyed an almost uninterrupted rally since the bull market began in October 2022, with the asset class on track to outperform other major asset classes for a third consecutive year. But stretched valuations on AI-themed stocks, which triggered a rotation out of technology and into small-caps last week, highlighted the vulnerabilities associated with investing in highly concentrated markets like the S&P 500 Index (SPX).

Morgan Stanley – “How Much Is Too Much?” – June 4, 2024

We recently shared how investors can achieve adequate diversification within the equity asset class by switching from the SPX to an equal-weighted index like the Invesco S&P 500 Equal Weight ETF (RSP). Another effective way to achieve adequate diversification is to build a multi-asset portfolio by adding other asset classes that may provide uncorrelated returns to equities.

In this article, we assess the potential for commodities to outperform amid growing anticipation that the Federal Reserve (Fed) will begin to unwind monetary policy in September. More importantly, we discuss why investors should be more selective when investing in commodities. Finally, we share our favourite picks within the asset class.

Commodities As An Asset Class

Before we begin our discussion about investing in commodities, let us set a few things straight.

Firstly, we point out that the financial media has a habit of overgeneralising commodities by lumping them together and treating them as a single asset class. This usually results in a superficial discussion of commodities and dilutes any analysis.

Although equities consist of companies that are broadly exposed to the same macroeconomic forces, such as monetary policy and aggregate demand, the forces driving demand and supply for a particular commodity could be starkly different from another. Indeed, the term commodities encompasses an entire array of traded goods that range from industrial materials such as metals, plastics, and crude oil to agricultural products such as wheat, coffee, and even livestock. The factors driving the prices of zinc may be completely unrelated to the factors driving the prices of cattle or orange juice.

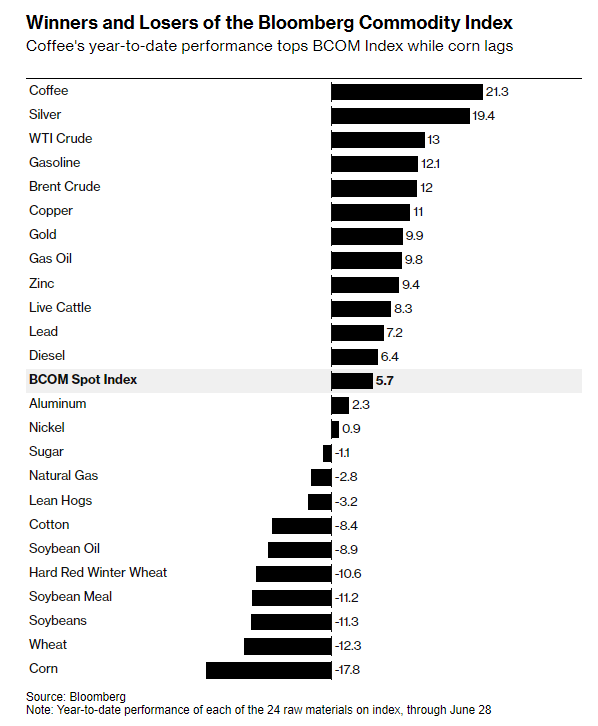

Even the performance of individual commodities can vary significantly from year to year. As we can see from the table below, there will be big winners and big losers in the commodity markets each year, and it is quite common to see prices swing in magnitudes of double-digit percentage points.

VisualCapitalist.com, Bloomberg, U.S. Global Investors

Secondly, because commodities typically do not generate returns over time in the form of earnings, interest, or rent, they are often viewed as an inferior asset class compared to equities, fixed-income, and real estate.

Advocates of commodity investing would argue that commodities have often shielded portfolios against losses during periods of high inflation and provided uncorrelated returns to equity over time. Meanwhile, commodity traders would also argue that the dramatic price swings unique to commodity markets regularly present attractive trading opportunities for outsized returns that dwarf that of other asset classes.

Lastly, at Stratos Capital Partners, we prefer to view commodities as goods that we do not plan to own or hold, but only to trade for speculative profit (buying and selling) in the form of derivatives. This is in stark contrast to investible asset classes such as equities, fixed income, or real estate, which we can legally own and hold to generate returns over the asset’s lifetime. One key difference is that trading profits from commodities come purely from changes in price, while other asset classes tend to generate some form of economic or contractual return over time.

A Mixed Performance For Commodities

Commodities have had a mixed performance in recent years, partly due to China’s sputtering economy and tight monetary policy across major developed countries.

As the following chart shows, the S&P GSCI Index, a production-weighted index constituting a globally traded basket of commodities, has seen a relatively flat performance while the SPX has been enjoying an almost uninterrupted rally over the past 12 months.

However, comparing the performance of the two asset classes over longer periods of time (three years), we can see that 2022 was an amazing year for commodities due to a sharp spike in prices for crude oil, natural gas, coal, and wheat. This was mainly due to the Russian-Ukraine war. Furthermore, commodities have also outperformed the SPX over the same period of time.

This outperformance of commodities during a year in which the S&P 500 Index plunged into a bear market highlights why most institutional investors maintain some moderate level of portfolio allocation towards commodities across market cycles. This exposure to exogenous events, as well as the idiosyncratic risks associated with individual commodities, help generate uncorrelated returns to other major asset classes and enhance portfolio diversification for investors. Indeed, many exogenous events that negatively impact the economy from time to time (such as war or a supply shortage of some critical commodity) tend to be overwhelmingly bullish for the prices of the affected commodity.

Instead of passively allocating a portion of the portfolio to a broad basket of commodities, most investors prefer to select a handful of commodities that they believe are likely to benefit disproportionately from some form of macroeconomic tailwind or industry-specific development. Although this is a more selective and research-intensive approach to commodities investing, we believe that being selective is absolutely critical for alpha.

One reason is that commodities as a whole have underperformed equities over much longer time frames. As the chart below shows, commodities have lagged far behind the S&P 500 over the past decade.

But that does not necessarily mean that commodity investing is simply not suitable for passive investors. Instead, we argue that there are periods during which even investing in a broad basket of commodities would make a lot of sense for passive investors.

Equity-Commodity Price Gaps Are At An Extreme

One of the most reliable factors for separating the winners from the losers in almost any kind of investing is valuation. And we argue that commodities as a whole have never been this cheap compared to equities since the 1970s.

Below is an infographic taken from VisualCapitalist.com, which shows that the ratio of the S&P GSCI Index versus the S&P 500 Index has reached an extreme low. More importantly, each time that ratio has reached extreme lows, it also signals the beginning of a new commodity supercycle.

VisualCapitalist.com

We see increasing evidence that we could indeed be entering a commodity supercycle over the next couple of years, and the odds are stacked quite favourably for the commodity bulls.

Because many of the world’s most liquid and widely traded commodities are priced in U.S. dollars, research has shown that commodity prices tend to rise during periods when the U.S. dollar depreciates against other major currencies. Therefore, as the Fed begins to unwind monetary policy in September, we may start to see moderate weakness in the U.S. dollar supporting commodity prices.

To be clear, we are entering an environment in which we are likely to see not just monetary easing in the U.S., but a more coordinated unwinding of monetary policy globally. Although this could mean that the U.S. dollar may not weaken by much, if at all, we are still likely to see global demand for commodities pick up meaningfully in the next one to two years.

Overall, we see ample scope for commodities to outperform as an asset class, especially given that valuations on the SPX remain stretched and priced for AI perfection. For passive investors looking to build exposure to commodities, the iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA:GSG)may be a suitable choice.

Picking The Winners

For investors looking to build a more selective and concentrated exposure to commodities, we have already warned that this could be a risky endeavour, given how wide the performance of individual commodities may vary. The chart below shows the year-to-date performance of various commodities as of 28 June.

Bloomberg

One way to be more selective is to pick commodities that we think are likely to outperform due to favourable demand-supply dynamics driven by industry-specific tailwinds.

Copper – Undermined Despite An Impending Shortage

One of our favourite commodity picks is copper, and the sharp decline in copper prices in recent weeks is once again presenting a compelling trading opportunity.

The core of our investment thesis on copper remains unchanged. We continue to see an impending shortage of copper due to acute underinvestment in developing new mines, and deteriorating ore grades at some of the world’s largest copper mines. Furthermore, we believe that future demand for copper has also been grossly underestimated due to the rapid electrification of the global economy. We continue to see a rapid build-out of energy-hungry data centres and an increasingly desperate need for renewable energy to drive growth in electric vehicles and in almost every form of modern industrial application. All of which would require new energy grids and infrastructure to be built or upgraded over the next decade. Copper will be a critical material in short supply.

To be clear, we have been bullish on copper since October 2022 and still think the metal has ample upside potential. Although we were admittedly surprised by the sharp sell-off over the last couple of weeks, we maintain our bullish view and would take this opportunity to add to our bullish positions on the Global X Copper Miners ETF (COPX) and Teck Resources (TECK).

Crude Oil – Trading Bullish Rebounds Within A Stable Range

Another of our favourite commodity picks is crude oil. However, we are taking a predominantly trading approach to crude oil rather than from an investing point of view.

The main reason for this is simply because we have identified a good technical trading range on WTI crude oil, and that we have taken several successful trades based on this setup. We think the trading opportunities for crude oil are just much more attractive compared to the fundamentals driving the commodity. So, although we generally maintain a bullish view on WTI crude, we prefer to trade the price action over much shorter time frames to maximise alpha.

To learn more about our WTI crude oil ideas, we encourage readers to check out our recent articles on the ProShares Ultra Bloomberg Crude Oil ETF (UCO) and to keep a lookout for new ones.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.