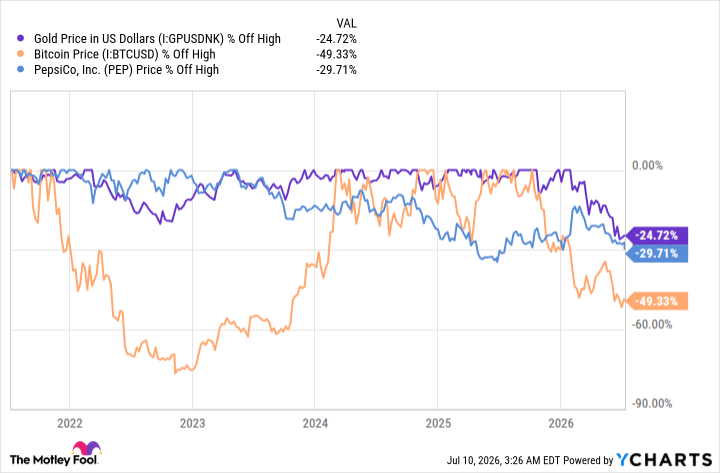

My big problem with gold and Bitcoin (BTC +1.27%) is that they aren’t operating businesses. An ounce of gold will always be an ounce of gold, and one Bitcoin will always be one Bitcoin. The value of either can only rise if someone else is willing to pay more for it. But right now, gold is down 25% from its recent high, while Bitcoin is down nearly 50%.

I’d rather buy one of the world’s largest consumer staples stocks while it is down nearly 30%. Not only has that drop pushed its yield up to 4.1%, which is historically high, but this food and beverage giant is already making changes to its business to get back on track. Here’s why I’d buy PepsiCo (PEP 0.35%) over gold and Bitcoin in July.

Image source: Getty Images.

Gold and Bitcoin have fallen out of favor

Investor sentiment is the driving force behind price movements on Wall Street. That’s as true of gold and Bitcoin as it is of PepsiCo. However, there’s a material difference between these investments. The only thing that gives Bitcoin value is people’s willingness to own it. Gold has some fundamental value as an industrial commodity, but its primary function in the world is as a store of wealth. Investors don’t seem to view gold and Bitcoin the way they did just a short while ago.

There are several reasons this could be the case. The economic outlook could have improved, reducing the need for a store of wealth. The price of gold and Bitcoin could have risen to the point where their value as a store of wealth no longer makes economic sense. Or investors could have just moved on to other investments, noting that Robinhood‘s (HOOD 2.77%) transaction-based revenue from cryptocurrencies fell 47% in the first quarter while revenue from prediction markets rose 320%.

Gold Price in US Dollars data by YCharts

PepsiCo’s price has fallen, too, because investors aren’t as interested in owning the stock. But there’s a deeper reason. The company isn’t performing as well as Wall Street was hoping. Management is working on the problem, adjusting its business to better serve consumer tastes. It is the same thing that PepsiCo has been successfully doing for decades. Being able to adjust and improve its business over time is how the company became a Dividend King, with over 50 consecutive annual dividend increases. It’s how the company grew to become one of the world’s largest beverage and food companies.

PepsiCo: Not great times, but they aren’t terrible either

PepsiCo just reported fiscal second-quarter 2026 earnings, and they were mixed. Revenues of $24.18 billion came in above Wall Street’s consensus estimate of $23.95 billion, but adjusted earnings of $2.20 fell a penny short of the $2.21 expectation. The stock fell a few percentage points on the news. Investors can get very upset about a penny or two, but miss the bigger long-term picture.

To be fair, there were some notable negatives. For example, while organic sales rose 2.4% in the quarter, that was driven by foreign markets. The North American food business saw organic sales drop 2%. And while North American beverage sales increased by 1%, volume decreased by 4%. North America is an important market for PepsiCo, so weakness in the region isn’t something to ignore.

Today’s Change

(-0.35%) $-0.48

Current Price

$137.38

Key Data Points

Market Cap

Day’s Range

$135.31 – $137.96

52wk Range

$133.75 – $171.48

Volume

9.1M

Avg Vol

8.1M

Gross Margin

53.98%

Dividend Yield

4.17%

That said, the company’s globally diversified portfolio offset the weakness in North America. That’s good news and shows why owning a large, diversified consumer staples company is a good idea for long-term investors. Moreover, the company continues to adjust its business to the current market environment, introducing new products such as protein chips and probiotic beverages. Gold and Bitcoin can’t do that.

PepsiCo’s dividend looks safe

Given PepsiCo’s long history of success and industry-leading brands, I’m confident it will muddle through this weak patch and get back on track. It has done the same thing many times before. Meanwhile, investors can collect a 4.1% yield while they wait. And, notably, the $1.48 per share per quarter dividend was more than covered by the $2.20 of adjusted earnings. So the dividend looks very safe. Neither gold nor Bitcoin pays you to stick around while you hope for higher prices.

It may take a while for PepsiCo to turn its North American business around. Indeed, even good businesses go through hard times. But the ability to adapt to the times is why I’d rather own PepsiCo than gold or Bitcoin in July. Of course, the well-above-market dividend yield helps, too.