November 2025 Stock Market Outlook: Key Takeaways

- Valuation increases surge in October, taking market valuation to a slight discount.

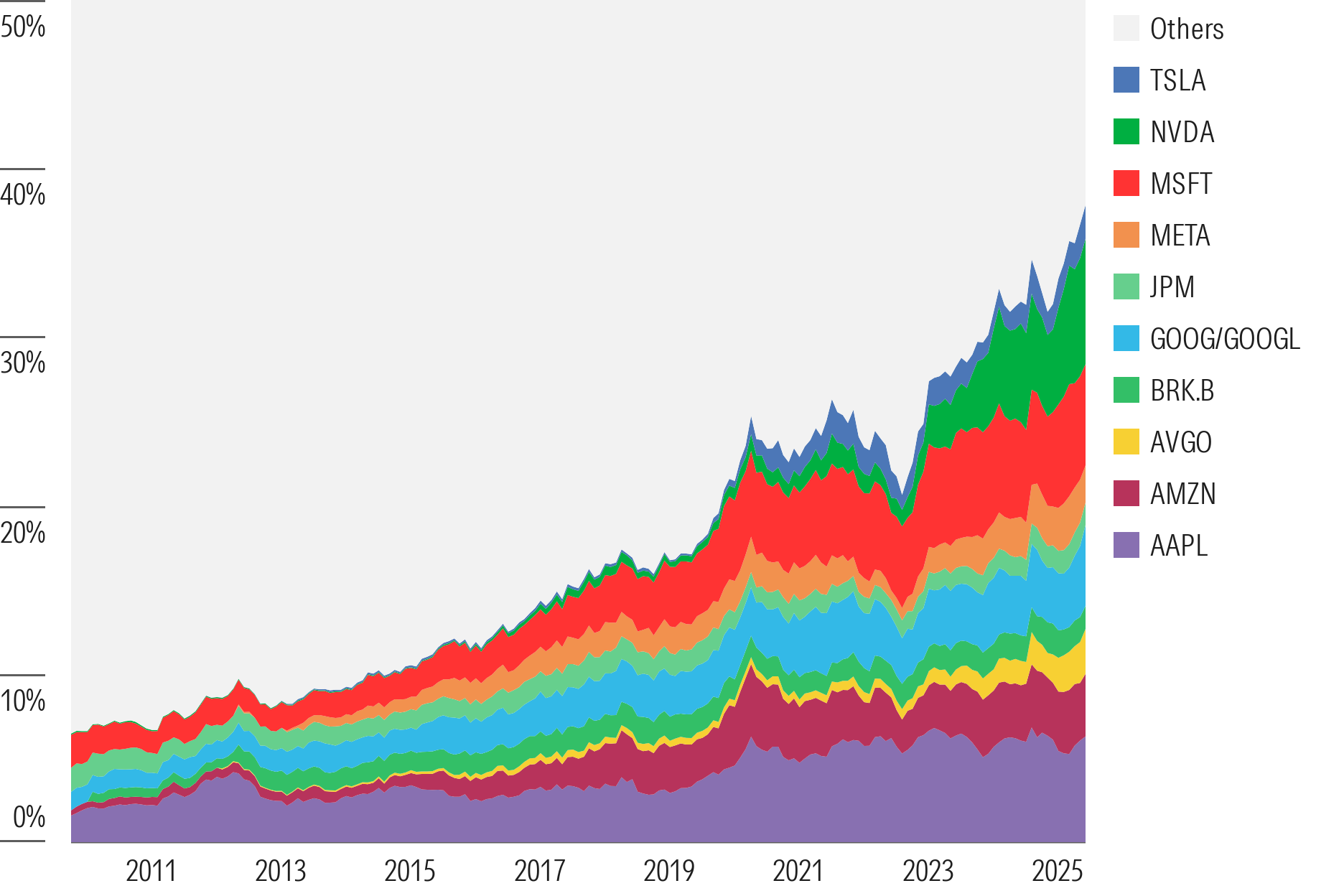

- Big gets bigger, and concentration becomes more concentrated.

- Style and sector dynamics: growth premium shrinks, small-caps attractive.

As of Oct. 31, 2025, the US equity market was trading at a 2% discount to a composite of our fair value estimates of the over 700 stocks we cover that trade on US exchanges. While the Morningstar US Market Index rose a healthy 2.21% in October, a composite of the market capitalization of those stocks under our coverage had risen even faster. In fact, the total market capitalization of our valuations rose by $4.2 trillion, which is over 5% of the market capitalization of the stocks we cover. By percentage of our coverage, over the course of October, we increased our fair values on over 20% of our coverage, outpacing the number of declines by a 3-to-1 ratio.

Year to date, the net increase across our valuations totaled $12.4 trillion, representing an almost 17% increase in the total capitalization of the stocks we cover.

Big Gets Bigger, and Concentration Becomes More Concentrated

The US stock market has continued to become increasingly more concentrated as the valuations of the largest of the mega-cap stocks become an increasingly larger percentage of the market. Not only is the market increasingly concentrated in only a few stocks, but eight of the 10 largest stocks by market capitalization are directly tied to the artificial intelligence buildout boom.

While the number of fair value increases far outpaced the number of decreases in October, only six stocks comprised the preponderance of capitalization increases. We increased our fair value on Alphabet GOOGL twice during October. The first time was after it announced a new partnership with Anthropic, and then following a stronger-than-expected earnings report. The total increase in market capitalization was $1.2 trillion. To put that in perspective, that’s greater than the market capitalization of Warren Buffett’s Berkshire Hathaway BRK.B, which is the tenth largest company in the stock market.

We increased our valuation of Nvidia NVDA by $800 billion after CEO Jensen Huang disclosed that the company expects $500 billion of cumulative sales in calendar 2025 and 2026, leading us to increase our revenue assumptions. To put that in perspective, that increase is equal to the market capitalization of Walmart WMT.

Following Apple’s AAPL earnings release, we increased our valuation by $440 billion, equivalent to the market capitalization of Johnson & Johnson JNJ. Rounding out our increases, we increased Broadcom AVGO by almost $200 billion, and increased Tesla TSLA by $167 billion. These increases are equivalent to the market capitalization of Home Depot HD.

The valuation increases for just these six companies equate to $3.1 trillion of the market capitalization. To put that in context, that’s equivalent to 31 companies with $100 billion market capitalization each. To further put that in context, there are only about 140 companies with a market capitalization of $100 billion or more.

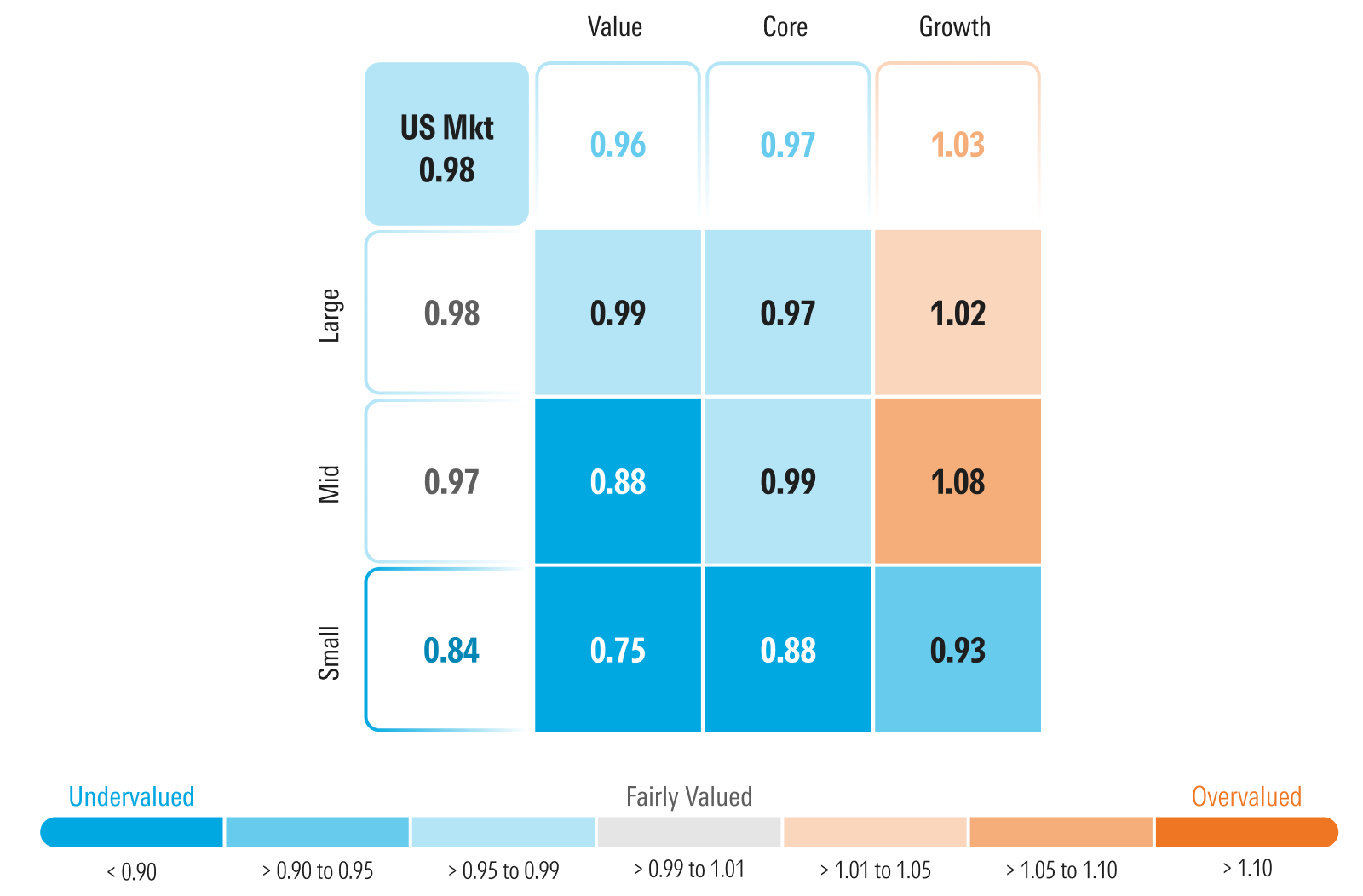

US Stock Market Trading at a Slight Discount

The Morningstar US Growth Index rose 1.42% in October. However, our price/fair value metric of the growth category declined to only a 3% premium at the end of October from a 12% premium at the end of September. The reason is that our valuation increases across our growth stock coverage well outpaced the amount that the growth index rose. While the growth category remains at a slight premium, we continue to see a number of attractive undervalued growth stocks such as Oracle ORCL and Workday WDAY. Value stocks remain the most attractively valued yet on a relative value basis to a lesser degree, following our valuation increases in growth. Core stocks’ valuations remain split between value and growth valuations.

As mega-cap AI stocks surged in October, the Morningstar Large Cap Index rose 3.09%. Yet, our price/fair value metric declined to a 2% discount at the end of October from a 4% premium at the end of September. The reason is that our valuation increases across our large-cap stock coverage well outpaced the amount that the index rose. On both an absolute value and relative value basis, small-cap stocks remain very attractive, trading at a 16% discount to our fair value estimate.

Beyond the Buildout: The Coming Pivot in AI Investment Strategy

Once again, this earnings season, it’s been all about the AI arms race and the buildout boom to develop new facilities and platforms as fast as possible.

Growth in spending on capital expenditures is still accelerating, and not only increasing in nominal terms, but also increasing as a percentage of a company’s revenues. In this race to capture the first-mover advantage, we are increasingly seeing these same companies tap the public bond markets to raise tens of billions of dollars to fund these buildouts.

While earnings results are idiosyncratic to individual firms, generally, what we have seen is that anyone tied to the AI buildout boom is exhibiting very strong growth rates. The fastest growth rates occurred in the technology, communications, and utilities sectors. However, for those firms that aren’t tied to AI, we have seen many sectors, such as energy, consumer, and real estate, stagnate.

While the markets’ focus through the end of this year will likely remain on who can build the most, the fastest, we suspect this focus will shift in 2026. Next year, we expect investors will turn their attention to identifying which companies will be able to utilize AI to improve their products and services and drive top-line growth. In addition, investors will look to those who can incorporate AI into their business processes to generate greater efficiencies and drive operating margins higher.

In the medium term, investors will also need to grapple with evaluating just how much new computing capacity will come online over the next five years and at what point will capacity start to outpace demand. To fully understand the longer-term economic value of AI, the market will need to better understand what the inference use cases will be, as opposed to current training use cases. At the end of the day, investors will want to see the economic value, path to profitability, and rates of return that will be generated on the voluminous amounts being spent on capital expenditures.

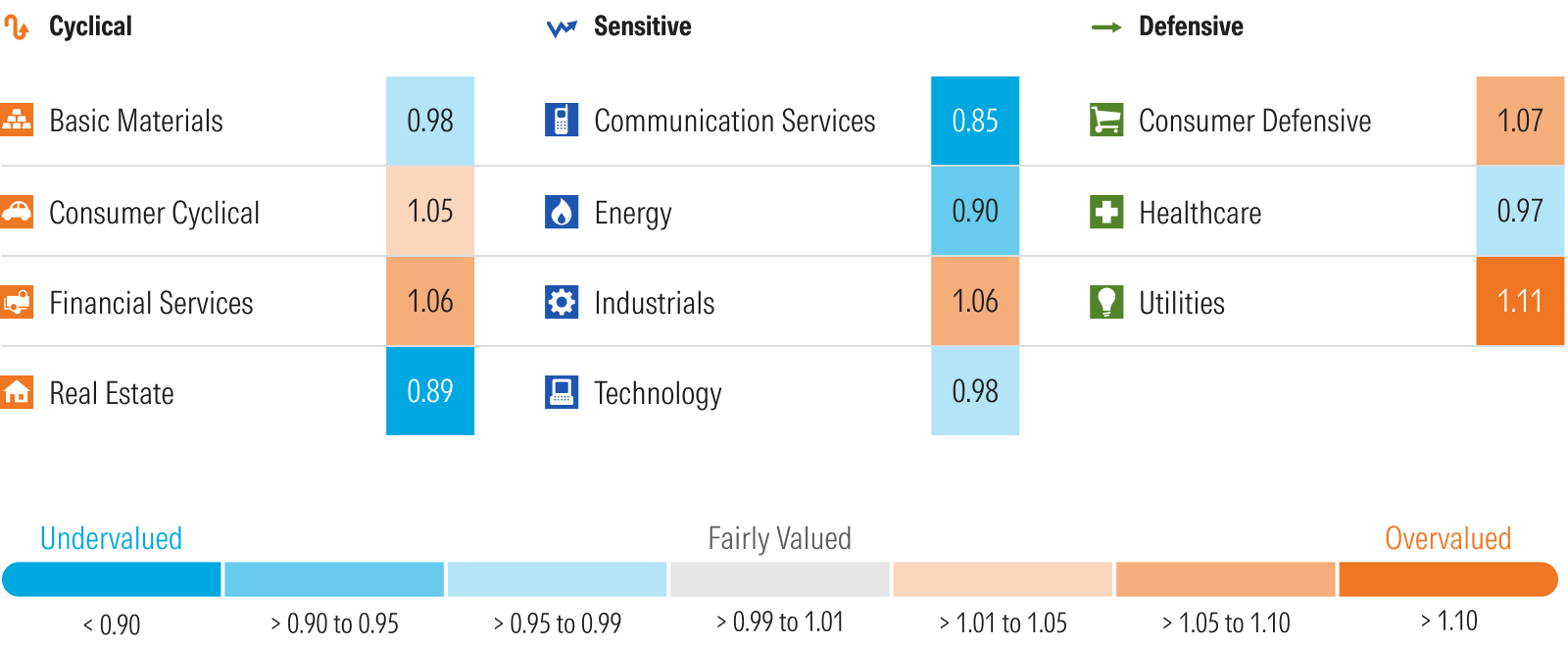

Undervalued Sectors

Communications

Communications regained the crown as the most undervalued sector. After increasing our valuation on Alphabet, the stock is now trading at about a 20% discount to fair value. Meta Platforms META sold off after earnings and is now trading at a 25% discount. These two stocks represent over 70% of the market capitalization of the sector, and as such, changes in their valuations disproportionally skew the overall sector valuation.

Real Estate

Real estate remains significantly undervalued. The Federal Reserve cutting short-term interest rates and long-term interest rates on a downward trend should provide a tailwind to valuations. We continue to prefer real estate with defensive-oriented characteristics and steer clear of urban office space.

Energy

Fundamentally, we think oil stocks are undervalued. In our valuation models, we use the market’s forward strip price for oil for the next two years and then our midcycle price forecast of $60/barrel for West Texas Intermediate crude oil. In addition, we think oil companies provide investors with a natural hedge in their portfolio if inflation were to stage a comeback or geopolitical risks were to push oil prices higher.

Overvalued Sectors

Utilities

The utility sector is broadly overvalued and offers few undervalued opportunities. While we incorporate heightened demand for electricity in our financial forecasts as AI computing requires multiple times more power than traditional computing, we think the market is overestimating too much growth for too long.

Consumer Defensive

The consumer defensive sector remains one of the most overvalued, yet the sector valuation is skewed into overvalued territory by 1-star rated Costco COST and Walmart. These two stocks are currently trading at over 50 times and 40 times earnings, respectively! That’s higher than the number of AI growth stocks we cover. Excluding these two stocks, the rest of the sector trades at an attractive 11% discount to fair value. We find stocks for packaged food companies to be particularly compelling.

Financials

According to our valuations, the sector is broadly overvalued. While banks will benefit from the Fed lowering the federal-funds rate and lower short-term borrowing costs will boost net interest income, we think the market is overestimating the amount of long-term earnings growth. In addition, better-than-expected economic performance has kept default rates and loan losses relatively low; we expect they will rise toward historically normalized levels as the economy slows. Insurance companies had been able to push through high premiums in the past few years, but we think this trend is coming to an end, and premium increases will subside.

Industrials

Considering we expect the rate of economic growth will decelerate sequentially over the course of 2025, we’d be especially cautious investing in industrials and require significant margins of safety to guard against slowing earnings over the short term.