Funtap/iStock via Getty Images

By Donn Goodman

Welcome back, readers. We are glad you have joined us. We hope that you are enjoying these longer summer days accompanied by the recent positive weeks in the stock market.

“The time has come for policy to adjust. The direction of travel is clear. My confidence has grown that inflation is on a sustainable path back to 2%.”

These were the words that Jerome Powell used on Friday at the annual conference in Jackson Hole, Wyoming. (I don’t think any of us could realize just how important the Jackson Hole conference has become). The stock markets positively reacted Friday with a sigh of relief. There had been somewhat of a negative anticipatory feeling on Thursday as many pundits grew concerned the Federal Reserve might not become quite as “dovish” as those words above indicate.

You will recall that two ½ years ago, the Federal Reserve embarked on an aggressive tightening policy to bring down inflation. The Federal Reserve hiked borrowing costs to crush pandemic-spurred inflation. Additionally, in 2021-2022, an acceleration in government spending and a curtailing of energy development exacerbated the situation, and inflation took a long time to start on a downward path.

Higher interest rates over the past 24 months have crippled many sectors of the economy, including home buying and borrowing for small companies that rely on regional banks for business expansion. The calls for the Fed to lower rates began in earnest late last year and have been repeated throughout 2024. But the Fed stuck to their guns and proclaimed that their overnight rates would stay “higher for longer.”

I guess us old timers in the market remember the 1970s all too well and how stubborn inflation can be to bring down. All of us as consumers (especially of rents and food) understand this recent cycle of inflation has been punishing. Many families in the US have a hard time being able to afford to put food on the table.

Mish and I have consistently said that the Fed should keep rates higher and avoid being premature in lowering them, thus spurring on potentially sticky and lingering inflation. In the face of them lowering rates to avoid a hard landing, the possibility of elevated pockets of inflation remains. I have covered some of these points and more the past two weeks in this column.

The Federal Reserve’s Job

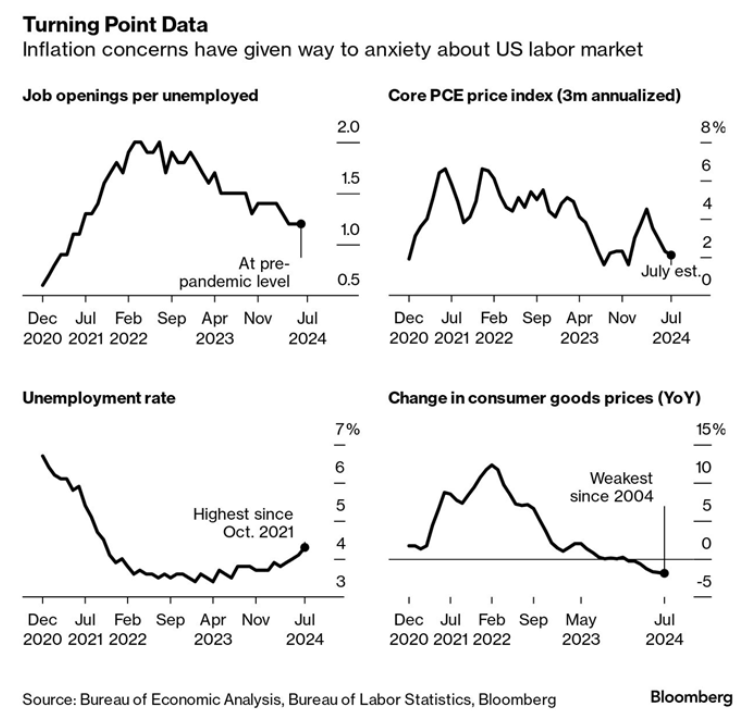

Just to rehash the Fed’s job here, they have a dual mandate to maintain price stability and to achieve maximum employment. Their view of whether interest rates should be increased or decreased is always dependent on the data. That said, there are now clear signs that the labor market is weakening, as it has recently risen to a 3-year high of 4.3% unemployment.

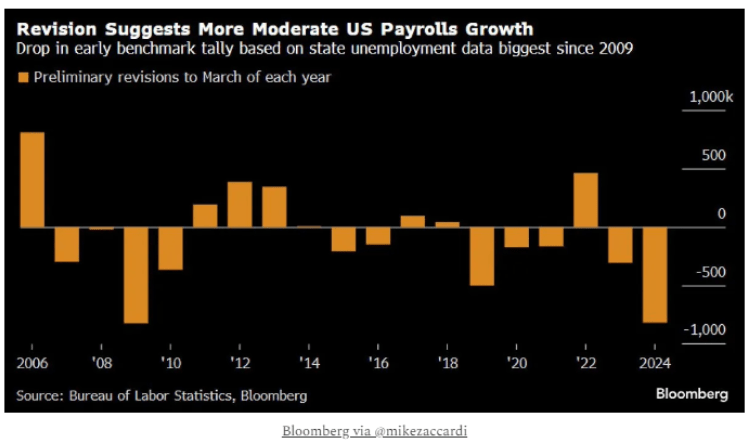

Additionally, this past week, the BLS (Bureau of Labor Statistics) revised job growth for 2024 downward (sharply). Jobless claims also jumped, and suddenly, the labor market looks a bit weaker than expected. See chart below:

BLS revisions. The preliminary revision showed 818k fewer jobs in the year through March than originally estimated. That brings the pace of job growth from 242k to 174k per month.

This was enough to convince the “data-dependent” Fed that it was time to move and a September rate cut is all but assured. The only question will be if it is the typical “first cut” of 0.25% or will the Fed get more aggressive and go 0.50%? Much of the Fed’s perspective and “data dependency” will be based on several important indicators to make their inevitable determination. See the Fed’s input variables below:

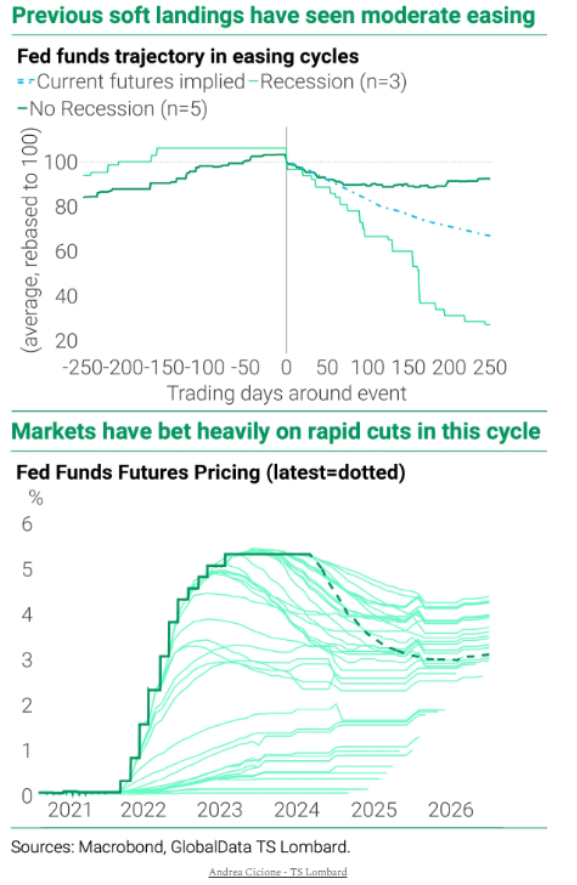

The stock and bond markets have been hanging on the anticipation that the Fed is ready to get more dovish and begin the lowering rate cycle. Odds that are in the futures markets currently show a reduction of 1.0% in the Fed Fund rates by year-end. Personally, with strong earnings, positive GDP and consumers’ still robust spending (see last week’s market outlook on retail spending), I wouldn’t take that bet. I would like to see 0.50-0.75% in a rate reduction. That would be a good start.

Typically, the Fed is gradual in the first rate cuts. However, the markets, as noted above, are expecting an aggressive reduction in rates by year-end, signaling a harder landing than anticipated. See charts below.

Fed vs. market. “Historically, the Fed has been relatively gradual in policy easing during soft landings, which contrasts with current market pricing.”

The markets

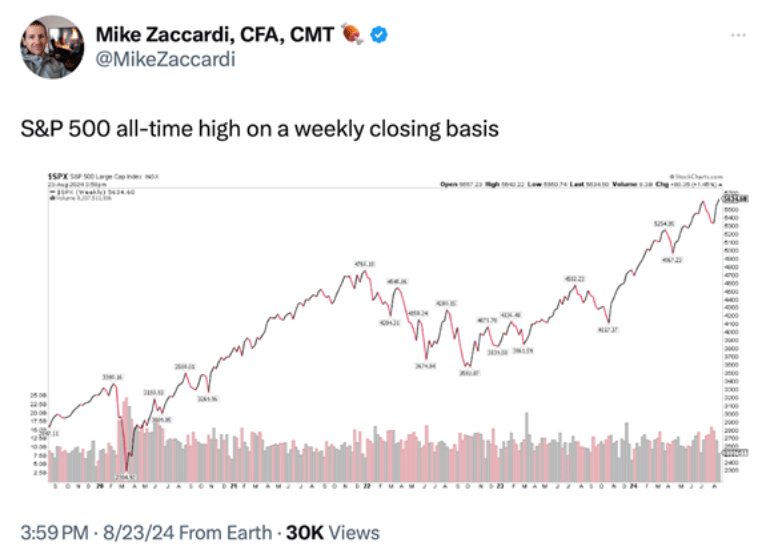

It was a good week for the stock and bond markets, as the S&P 500 had a new closing-week high (up 1.4% for the week, similar to the DJIA. The tech-heavy QQQ was the weakest of the 3, only up 1.0%). See chart below:

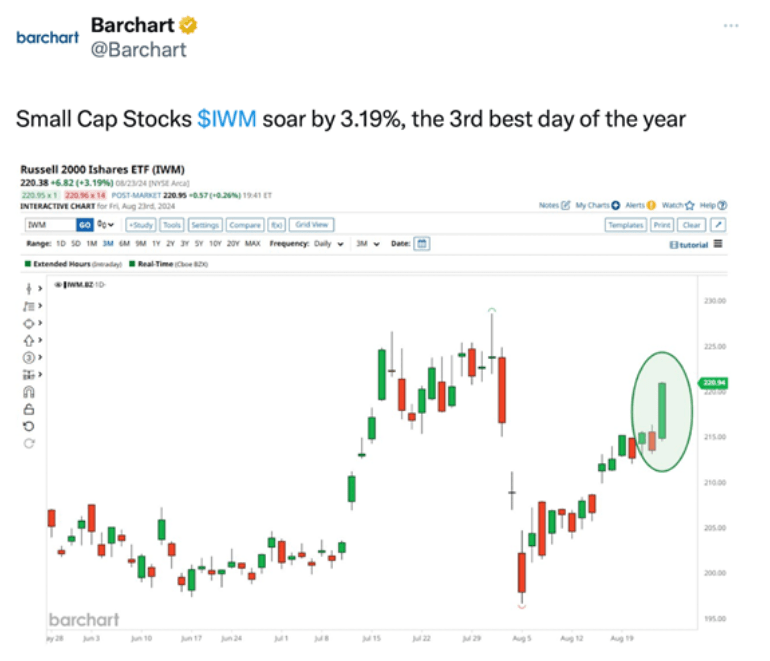

The big winners this past week were small-cap stocks, as the IWM (Russell 2000) was up over 3.0% for the week. This is one of the areas of the market that will benefit most from a reduction in borrowing costs. See chart on the IWM from Friday below:

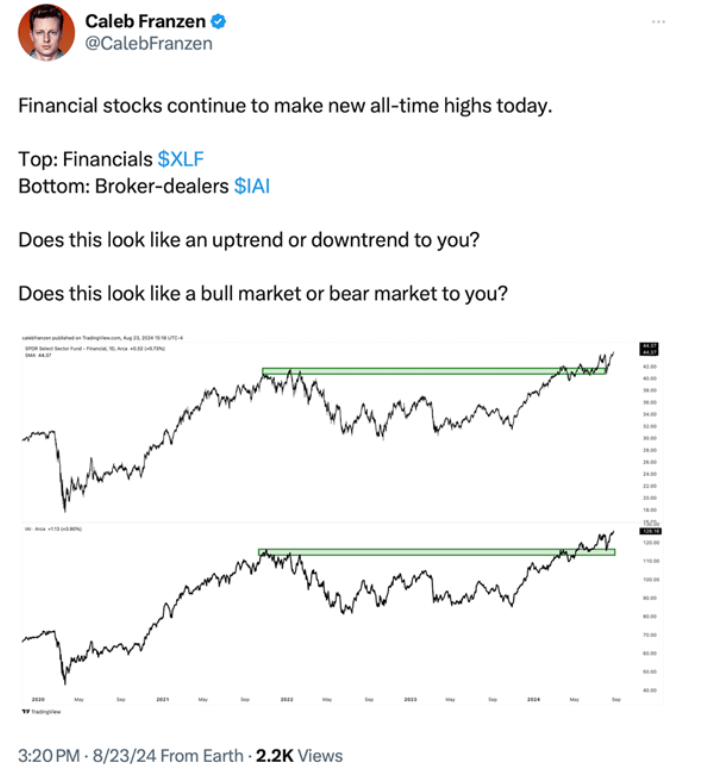

Homebuilders had a positive week as investors plowed money into financial stocks with the caveat that borrowing will pick up and home mortgages will accelerate. Given the stock market’s impressive move thus far in 2024, brokerage firms also accelerated to new highs. See charts that follow:

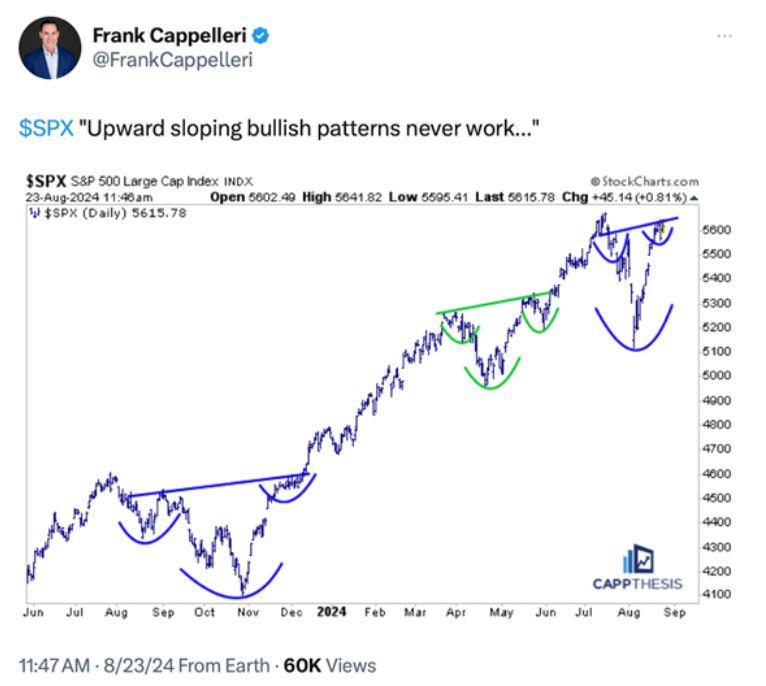

And a bit of sarcasm in the below chart as the S&P 500 sets up for a continued bullish move higher. See illustration below:

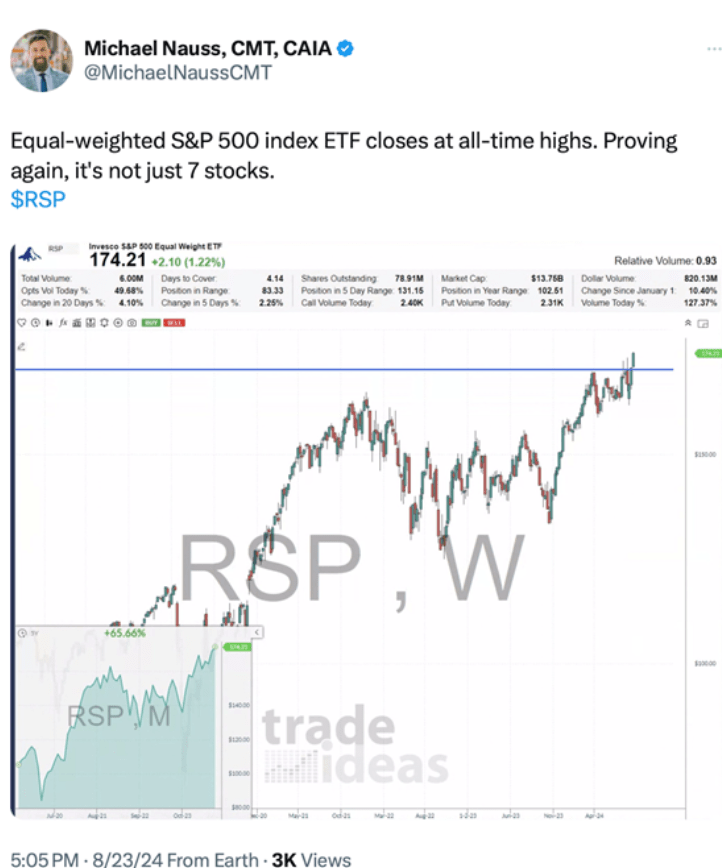

A much more broad participation in the markets. The recent rally in the S&P 500 has been broad-based and not all about the Magnificent 7. In fact, the stock market’s price appreciation has seen many underperforming areas of the markets that are now “catching up”. See chart below to exemplify this:

This recent broadening out of the stock market is a positive sign. The equal-weight S&P 500 (RSP) broke out to new highs this past week. See the summary and chart below:

- The S&P 500 (cap-weighted) remains only -0.6% below record highs. The equal-weight S&P 500 (RSP) is already there. This is evidence of a broad and healthy market.

- The Magnificent 7 (see note above) led the S&P 500 during the first leg of this bull market, but we’re finally seeing strength broaden out as the bull market matures.

- Breadth has been one of the biggest concerns throughout 2024, but participation has now dramatically improved.

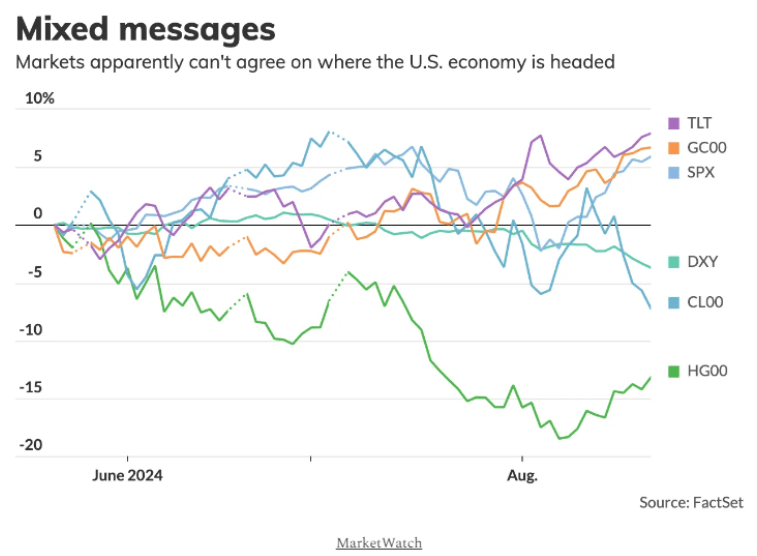

Yet, the markets are giving off some “mixed messages” as they wrestle with an economy that might enter a hard landing (recession) or, hopefully the Fed can thread the needle and orchestrate a soft landing going forward. See the mixed signal chart below:

Mixed messages. Surging stocks suggest a soft landing, rising bonds and gold signal a hard landing, falling prices for economically sensitive oil and copper point to weak global growth, and a lower USD raises doubts about international investor confidence.

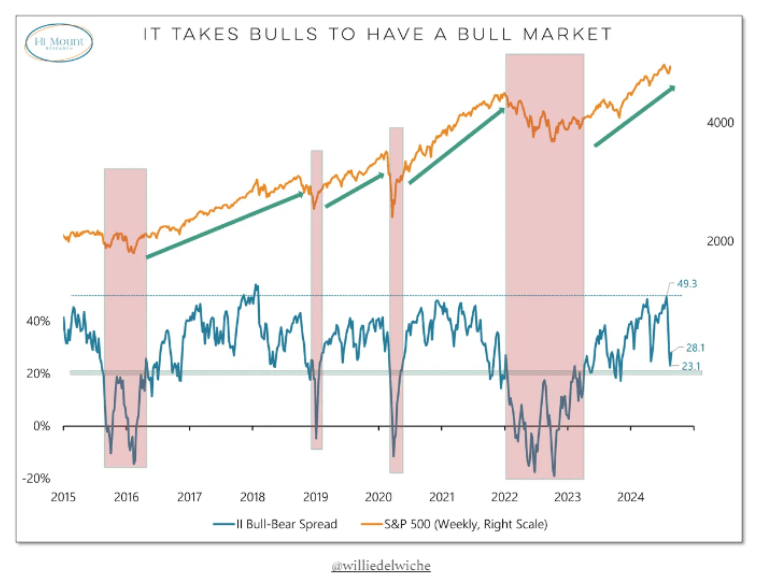

Investor sentiment remains bullish. See below.

Investor Intelligence. “50% bulls, 22% bears. Bull-bear spread rose for the first time in 4 weeks. Sentiment has been reset but optimism remains intact. That’s bull market behavior.”

I now turn it over to Keith and his team and the Big View bullets that follow.

As always, thank you for reading. Hopefully, you had a profitable week and enjoyed the positive market moves. Take care and good luck in your investments in the upcoming week ahead.

Risk-On

- Markets were positive on the week led by the Russell 2000, which had a banner day on Friday. Both the S&P and the Dow had their highest weekly closes ever. (+)

- Volume patterns confirm the positive move across all the indices. (+)

- Value is leading growth on a long and shorter-term basis, though both are in bull phases, which is considered bullish. Growth stocks are still leading the S&P. (+)

- 13 of the 14 sectors we follow were up, led by home builders (XHB) which benefited from the prospect of the Fed lowering rates. Consumer discretionary outperformed consumer staples. (+)

- Looking more at the global macro perspective, Clean Energy (PBW) and the metals (DBB) led, gaining on the possibility of lower rates. (+)

- Risk gauge improved back into risk-on readings. (+)

- The McClellan Oscillator for both the S&P and NASDAQ is back in strong positive territory, confirming the broader market move up.

- The cumulative Advance/Decline line is hitting new highs. (+)

- 52-Week New High New Low ratios for both NYSE and NASDAQ 100 are flipping positive. (+)

- The color charts – which looks at the moving average of the percentage of stocks over key moving averages – have moved into bullish mode across the board. (+)

- Looking at the percentage of stocks over key moving averages, on a short-term basis, S&P and IWM are looking overbought, though they are improving over a medium-to-long term basis. (+)

- Five of the six modern family members closed in bullish phases led by Regional Banks (KRE) on Friday, up over 5%. Semis were up on the week but remain in a strong warning phase, potentially signaling a passing of the baton onto other industries or sectors. (+)

- Emerging markets confirmed their bull phase, while more established equities exploded and closed on new all-time highs. (+)

- Soft commodities (DBA) and copper (COPX) regained their bullish phases this week. (+)

- With the prospect of the Fed lowering rates, the dollar is under pressure and the euro has hit its highest levels in over a year and over its 200-week moving average for the first time since mid-2021. (+)

- The short-end of the yield curve rallied off of sentiment that the Fed would be cutting rates. Equities could roar if economic data holds up. (+)

Neutral

- Market sentiment, as measured by VIXY, has reversed the huge spike as if the dramatic sell-off from early August never happened. The cash index VIX.X remains elevated from its extreme lows over the summer. (=)

- Gold closed on new weekly all-time highs and still looks very strong. (=)

- S&P and NASDAQ have unresolved bearish engulfing patterns from Thursday that need to resolve to the upside. (=)

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.