Yet beneath these strengths, a broader slowdown is settling in. Manufacturing has contracted for eight straight months, investment has recorded its steepest drop since 2020, and exports, long a pillar of growth, shrank in October. Domestic consumer confidence remains weak, reflected in sluggish retail sales.

In past downturns, markets looked to Beijing for heavy stimulus to steady growth. This time, that reassurance may not arrive.

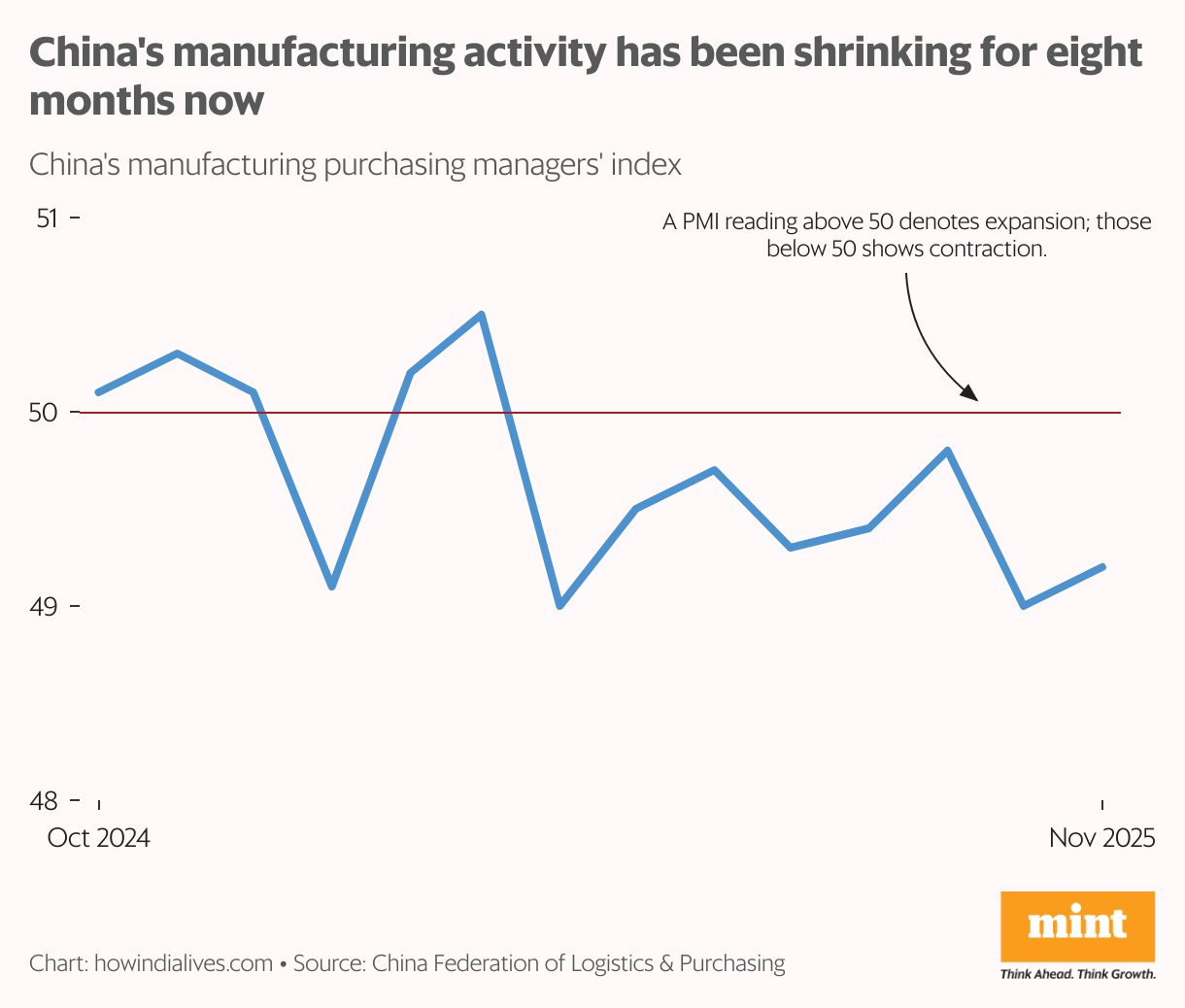

Plateauing production

Manufacturing, for long China’s growth engine, has stayed in contraction for eight consecutive months. The official purchasing managers’ index stood at 49.2 in November, below the 50 mark that separates expansion from contraction.

The private RatingDog survey, which tracks smaller export-focused firms, also slipped into negative territory at 49.9, down from 50.6 in October. Actual factory output was flat, with the production sub-index holding at 50.

The slowdown is also evident in the financial health of industrial firms (those with annual revenue above CN¥ 20 million). Their profits fell 5.5% year-on-year in October, driven largely by “involution,” the official term for cutthroat price competition caused by overcapacity. With margins squeezed, manufacturers cut staff for a fourth straight month and ran down finished-goods inventories at the fastest pace in nearly three years.

There were pockets of resilience. High-tech manufacturing expanded for a tenth straight month, with a reading of 50.1 in November. But the gains were too narrow to offset the wider slowdown.

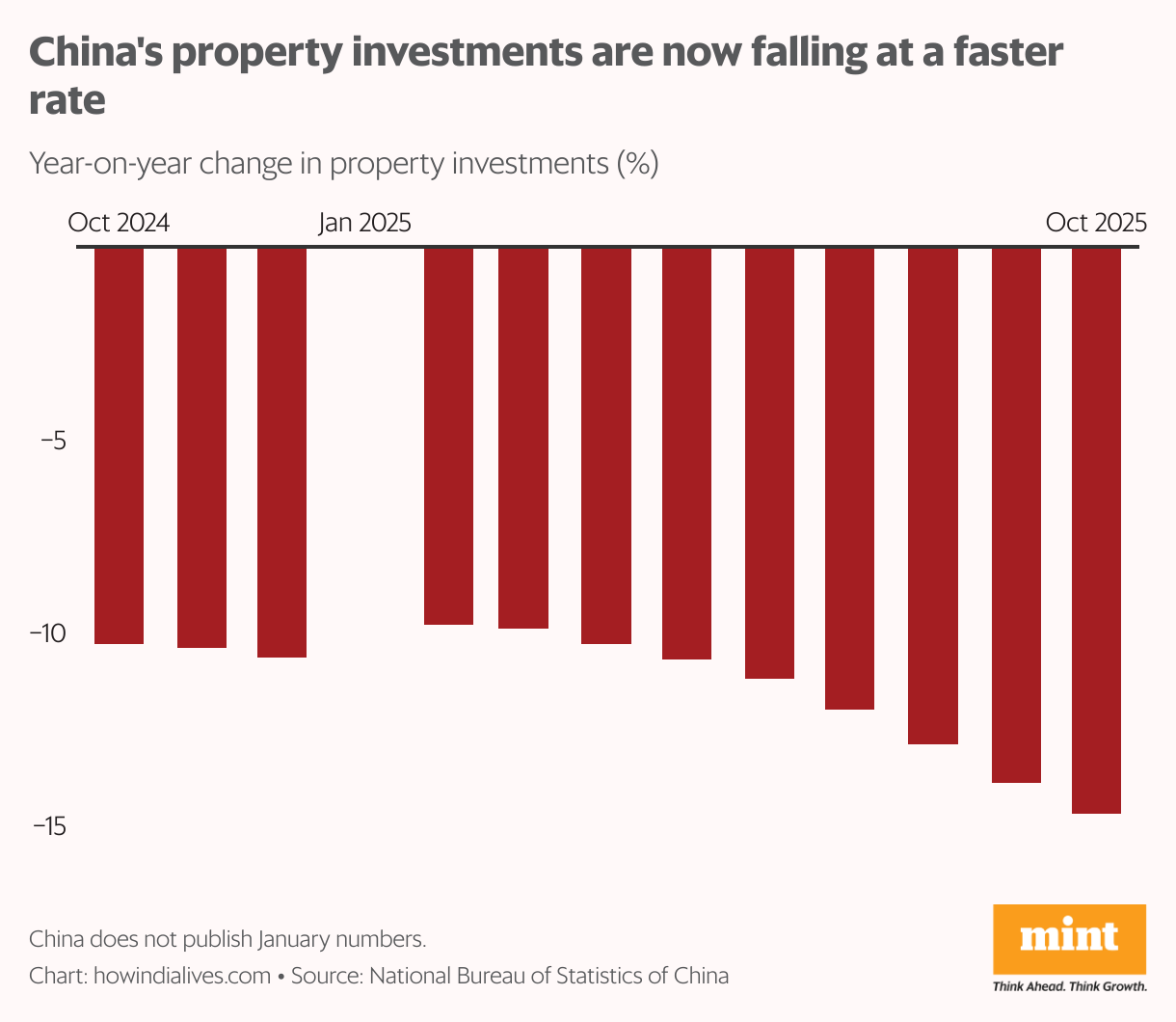

Capital retreat

China’s investment machine is also losing momentum. Fixed-asset investment fell 1.7% year-on-year in the first ten months of 2025, with October alone seeing an estimated 11.4% slump, the steepest drop since the 2020 lockdowns.

The biggest drag came from the property sector, where investment declined 14.7% as insolvent developers halted projects and new-home sales froze. Secondary home prices across 100 cities dropped nearly 8%, eroding household wealth. Even manufacturing investment, usually a reliable growth driver, grew just 2.7% through October.

The slowdown is tied largely to the government’s “anti-involution” effort, which restricts credit to saturated industries like EVs and solar to curb price wars and overcapacity.

Infrastructure spending also stagnated, contracting 0.1% year-on-year in the first ten months, as local governments diverted stimulus funds toward repaying heavy debts rather than launching new projects. Foreign businesses pulled back as well: utilised foreign capital fell 10.3% despite a rise in registrations.

Some analysts note that part of the decline may reflect statistical corrections to earlier over-reporting, but the broader trend is clear: China’s traditional growth drivers are weakening.

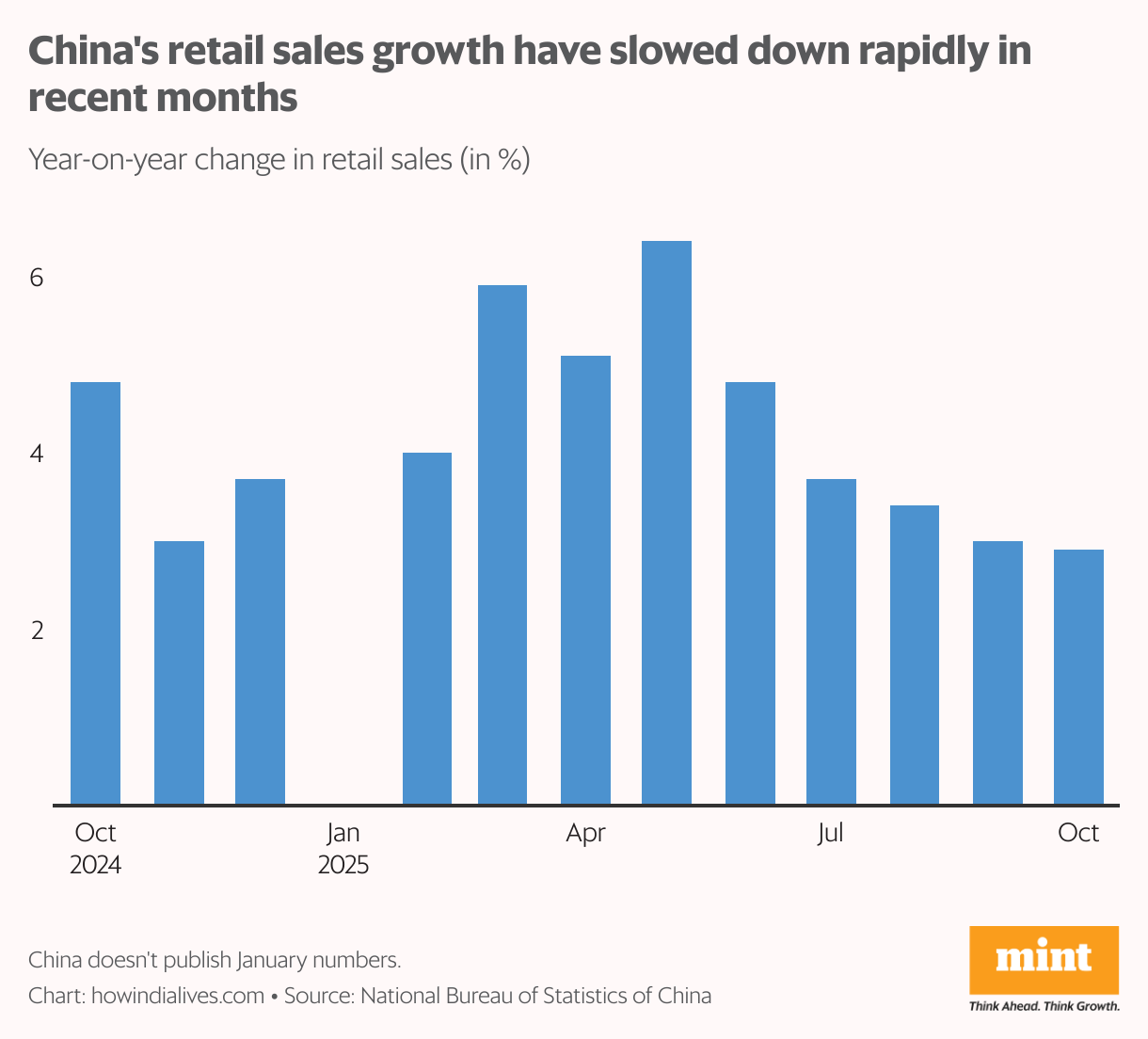

Consumer caution

Household spending has offered little relief. Retail sales grew just 2.9% in October, the slowest pace in over a year and the fifth consecutive month of deceleration. Auto sales shrank 6.6%, largely due to a “payback” effect: the government’s trade-in subsidy programme, launched in mid-2024 and expanded in 2025, pulled forward purchases, and the comedown showed up in October.

While there were outliers—Apple’s China smartphone sales rose 37% in October, and Tesla’s China-made electric vehicle (EV) sales grew 9.9% in November—overall appetite for big-ticket items remains weak.

Underlying this is a deep erosion of consumer confidence. Households are hoarding cash, pushing the total household deposits to about 120% of GDP (in the first half), largely because the property downturn has damaged their main store of wealth. Secondary home prices fell nearly 8% in November, and consumers have cut discretionary spending.

Some analysts point to a “deflationary mindset,” with buyers delaying purchases in anticipation of lower prices, compounded by anxiety over a weak labour market. There is growing concern that the consumption slump may continue to weigh on growth.

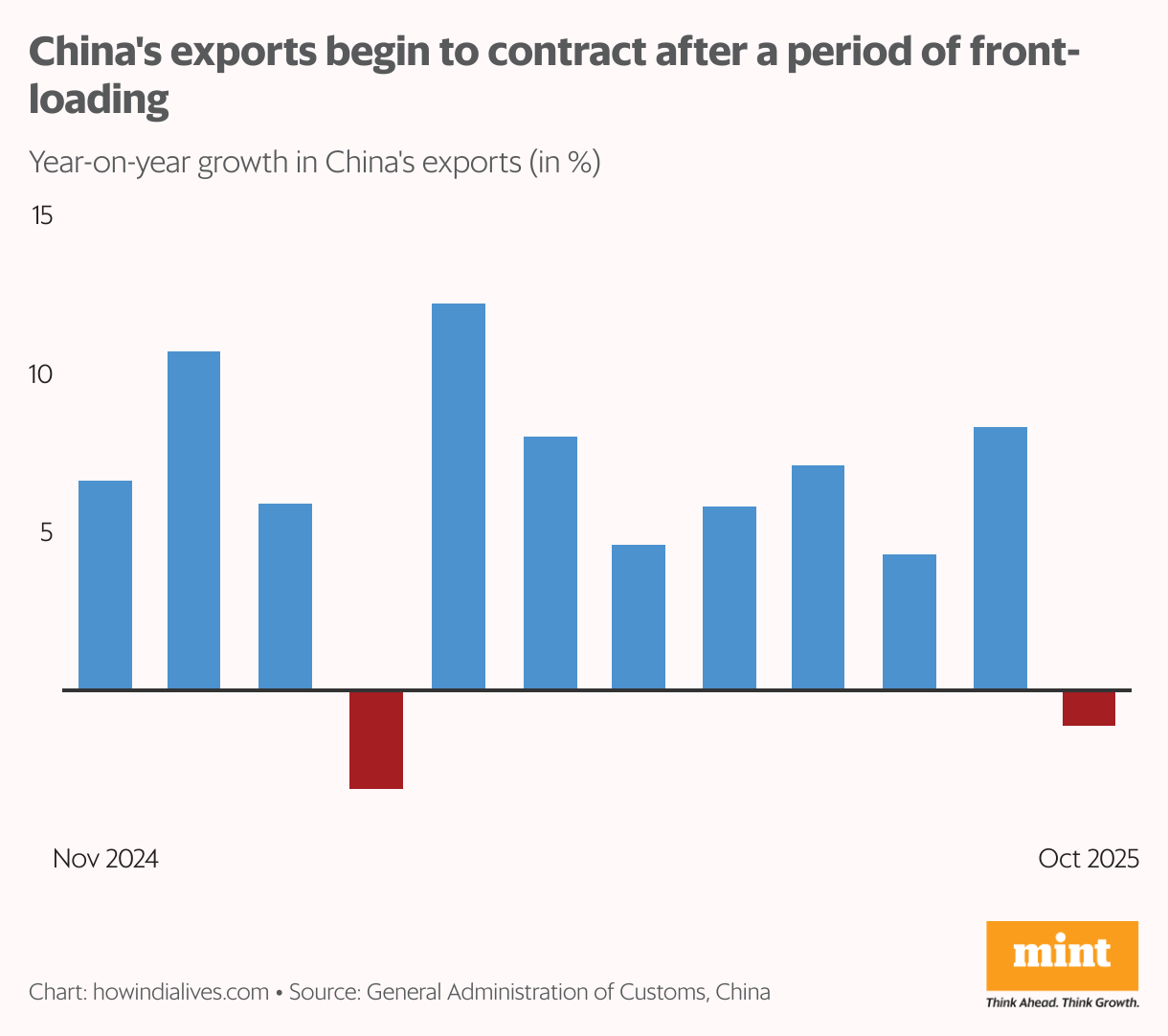

Trade turbulence

China’s external sector faced unexpected volatility in October as exports fell 1.1% in dollar terms. The drop followed a period of “front-loading,” when manufacturers rushed shipments to get ahead of US tariffs, leaving a gap once inventories were depleted. Shipments to the US plunged, but exporters redirected aggressively to other markets, with sales to Southeast Asia and Africa rising by double digits.

As a result, the annual trade surplus is still on track to exceed a record $1 trillion, driven by manufacturers offloading inventory abroad to weather the domestic slowdown.

Imports, meanwhile, grew only 1% in dollar terms, underscoring the ongoing weakness in domestic demand for global commodities. Despite the October slump, the outlook brightened modestly in November after a trade truce reached in South Korea paused rare-earth controls and resumed US soybean purchases. The diplomatic breakthrough helped push new export orders to an eight-month high, though the recovery remains fragile.

Painful pivot

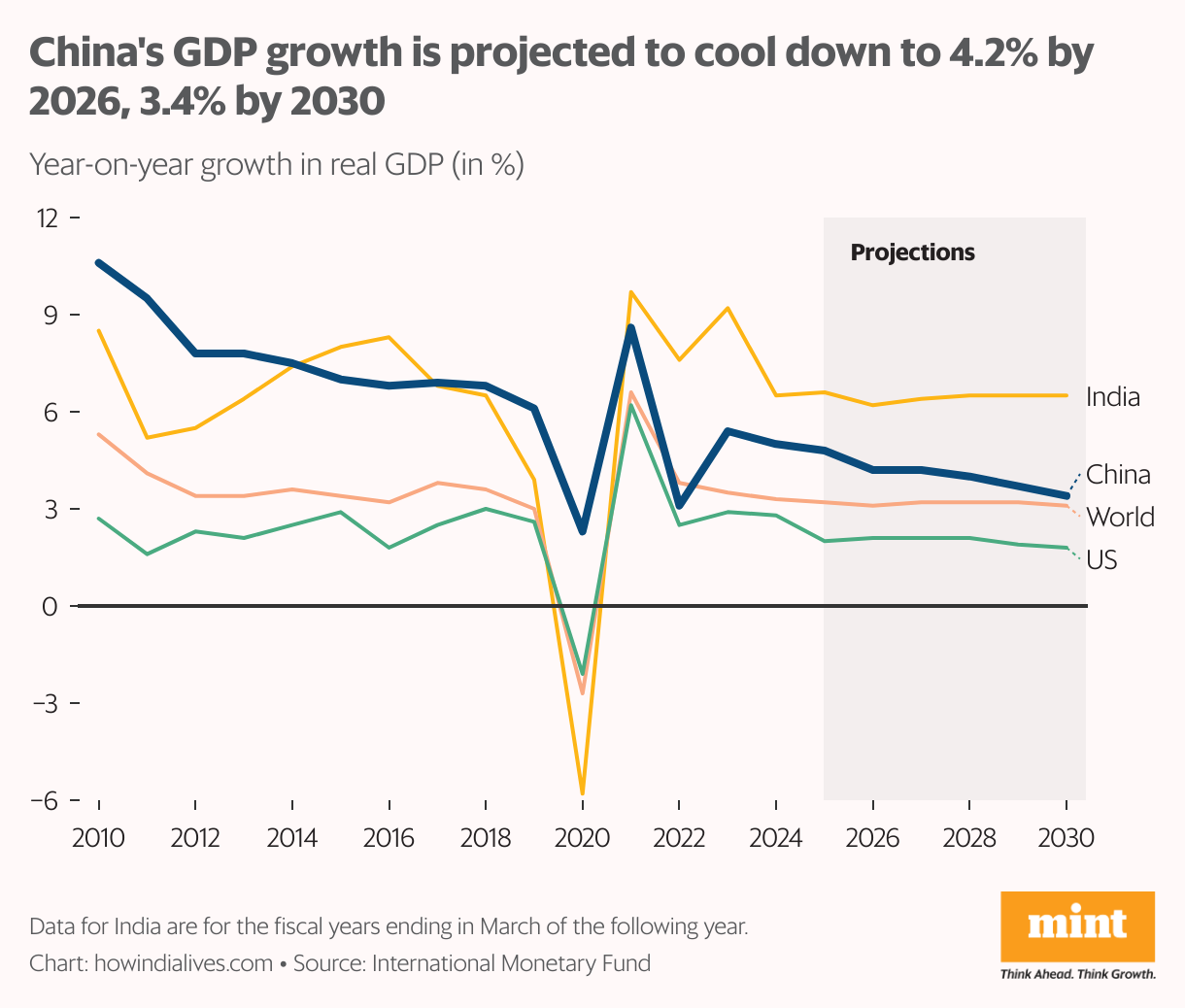

The International Monetary Fund (IMF) projects China’s GDP growth at 4.8% for 2025, unchanged from earlier estimates, despite heightened US tariffs. However, a moderation is likely from next year. It projected growth to slow down to 4.2% by 2026 and 3.4% by 2030. It warned of downside risks, including deflationary pressures, weak domestic demand, and vulnerabilities in the property sector, now four years into its downturn, which continue to weigh on financial stability and credit quality.

China’s Premier Li Qiang earlier said the country’s economy will surpass 170 trillion CN¥ ($23.87 trillion) by 2030, framing it as a major global opportunity. Achieving that target would mean an annual nominal growth of 4-5%. To get there, Beijing is rapidly pivoting toward “new productive forces,” prioritizing high-tech sectors such as AI, green energy, and advanced manufacturing over the debt-fuelled property expansion of earlier years.

That transition lies at the core of the government’s anti-involution drive, which restricts investment in saturated industries to curb wasteful price wars, and it is proving costly in the short run. Investment is slowing, consumption is soft and production is plateauing, and indications suggest those pressures may persist into 2026.