On 5 December 2022, Singapore-based commodity trader Trafigura signed a US$3bn loan agreement guaranteed by the German government to secure gas supplies when the Russia/Ukraine crisis triggered energy security concerns. The syndication was oversubscribed with 25 banks participating in the award-winning export credit agency (ECA) deal.7 This, together with the Gunvor €400m LNG agreement with Italian ECA SACE8 were examples of how governments are using an existing structure – ECAs – to avert the risk of market distortion in the bid to ensure certainty of energy supplies.

This spirit of collaboration between ECAs, commodity traders and financial institutions has since gathered momentum, said TXF Reporter Ralph Ivey in his introduction to the panel session comprising Oliver Schenkenberg (Gunvor), Yannick Luce (BGN); Maria Maliniemi (Finnvera) and James Lowrey (SMBC).

“Traders are continuing to deploy their liquidity on strategic acquisitions”

Panelists agreed that ECAs are now focused on developing access to supply chains for their exporters. The next growth area for ECA involvement could be soft commodities such as agricultural products, particularly for countries with strong domestic food distributors. Producers could also benefit as governments consider establishing funds to invest in metals.

Helped by sizeable profits in recent years that allows for more flexibility, larger traders are securing their supplies by lending to smaller companies unable to access bank liquidity. In response to a question from the floor to the ‘Keynote traders panel”, as to whether traders were the “new banks”, one panelist responded that while some traders were awash with cash with low utilisation of banking lines, “this could all change again in three years.”

Traders, however, are continuing to deploy their liquidity on strategic acquisitions – investing in physical assets to control price and supply chain risk. Two examples featured in trade press rooms included Trafigura’s South Korean nickel refinery (December 20239) and Mercuria’s US Gulf Coast energy storage assets (June 2024).10 In addition, Vitol extended its presence in the renewable energy market via its acquisition of BioMethane partners in April 2024.11

Across the 150 commodity finance transactions logged by TXF in 2023 totalling US$128.78m; oil and gas remains the dominant sector, notes Ivey in his report summary, “until a fundamental shift in energy demand take place” with traders and producers unlikely to see any kind of reduction in demand for these products “as developing countries grow”.12 This can hardly be a surprise given that access to energy, food staples and healthcare products top the import lists of economies climbing out of poverty or recovering from crises such as default or geopolitical conflict.

Furthermore, given that most renewables energy projects are not categorised as commodity finance, the barometer of demand and supply of clean energy is determined by the number of clean energy projects being financed (either through project finance or export credit agency deals) – and the minerals and metals being used to make them happen.

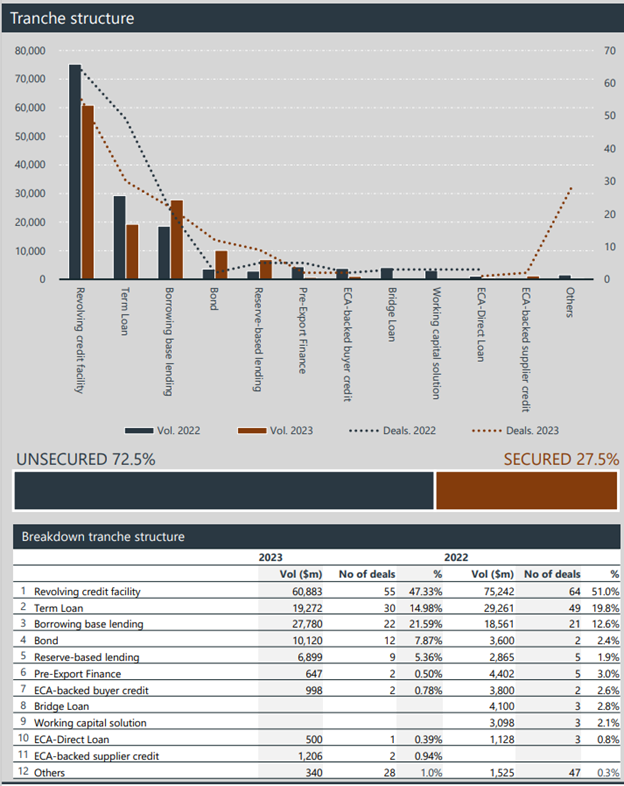

Figure 2: Breakdown of lending tranche structure

Source: TXF Commodity finance full year report 2023

Although the value and number of revolving credit facilities (RCFs) in the 2023 table had reduced in 12 months with borrowing base lending and reserve-based lending having risen, RCFs still comprise 47% of all lending. This surprised some of the ‘Global heads reunite’ financing panelists. “Around 10% of our limits are RCFs with 90% secured transactional financing of trade – going up to large traders as well”, was one comment.

Deutsche Bank’s Willem Calame and Rabobank’s Michiel Teunissen reflect on the shape of commodity finance transactions