")

Justin Paget

Investment Thesis

Vistra (NYSE:VST) shares have surged this year (up a staggering 106.31% YTD) through a combination of strong demand for power and the strong growth of AI and data center energy needs. Vistra’s stock in part has posted an incredible gain this year because of their completed integration of Energy Harbor and the power company’s expansion of their nuclear capabilities. The energy conglomerate feels confident in meeting the growing demand for clean, reliable energy, especially for supplying data centers, which are expected to see an exponential increase in energy consumption in the coming years.

Driving the market’s enthusiasm is Vistra’s diversified energy portfolio, particularly its nuclear assets. Analysts have been bullish, with many placing high price targets on the energy company due to the company’s strong earnings visibility and this anticipated growth in power needs from AI. While some analysts are more concerned, noting a potential oversupply risk for power, I’m personally not too concerned.

While Vistra is playing a secondary role in the AI revolution by supplying power, the company also has leveraged AI internally within their power plants by improving thermal efficiency and reducing carbon emissions. The company’s AI initiatives, such as the Heat Rate Optimizer (HRO), have allowed it to save millions in operational costs while making them a more attractive option for data centers seeking reliable, clean energy sources.

Following their strong 2Q report, I think the stock continues to trade at a relatively low price-to-earnings (P/E) ratio for a company with such growth potential. This valuation discount is striking, especially considering Vistra’s strategic positioning in the AI-driven power demand sector, which has led to a strong performance for what is traditionally viewed as a utility stock.

Q2 Results (Vistra)

In many ways, Vistra offers a strong combination of Utility level stability and dividends, combined with the growth potential we’d often associate with tech stocks. Their disciplined response to the growing demand for clean energy from data centers and other AI-intensive industries is promising.

Given this, I think Vistra is a compelling strong buy.

Company Is Firing On All Cylinders, They Have A Plan

Before I dive in, I want to note that while Vistra provides power in 20 states (and the District of Columbia) most of this research will focus on how their business will be impacted in Texas due to their scale there and this also being the spot I think they are set to see incredible growth.

During the company’s 2Q earnings call, management highlighted their strong financial performance and emphasized the growth trajectory in the utility sector. CEO Jim Burke pointed out that their ongoing operations adjusted EBITDA reached $1.414 billion, representing a 40% year-over-year improvement. The full integration of Energy Harbor’s assets contributed immensely to earnings in the last quarter alone. Burke noted:

Our 2024 results for generation of retail have benefited from the inclusion of the former Energy Harbor businesses, which benefit totaled approximately $200 million for the second quarter and approximately $260 million year-to-date. The contribution from these businesses for both the second quarter and year-to-date results was primarily driven by the PJM nuclear fleet, which accounted for approximately three quarters of the contribution in both periods -Q2 Call.

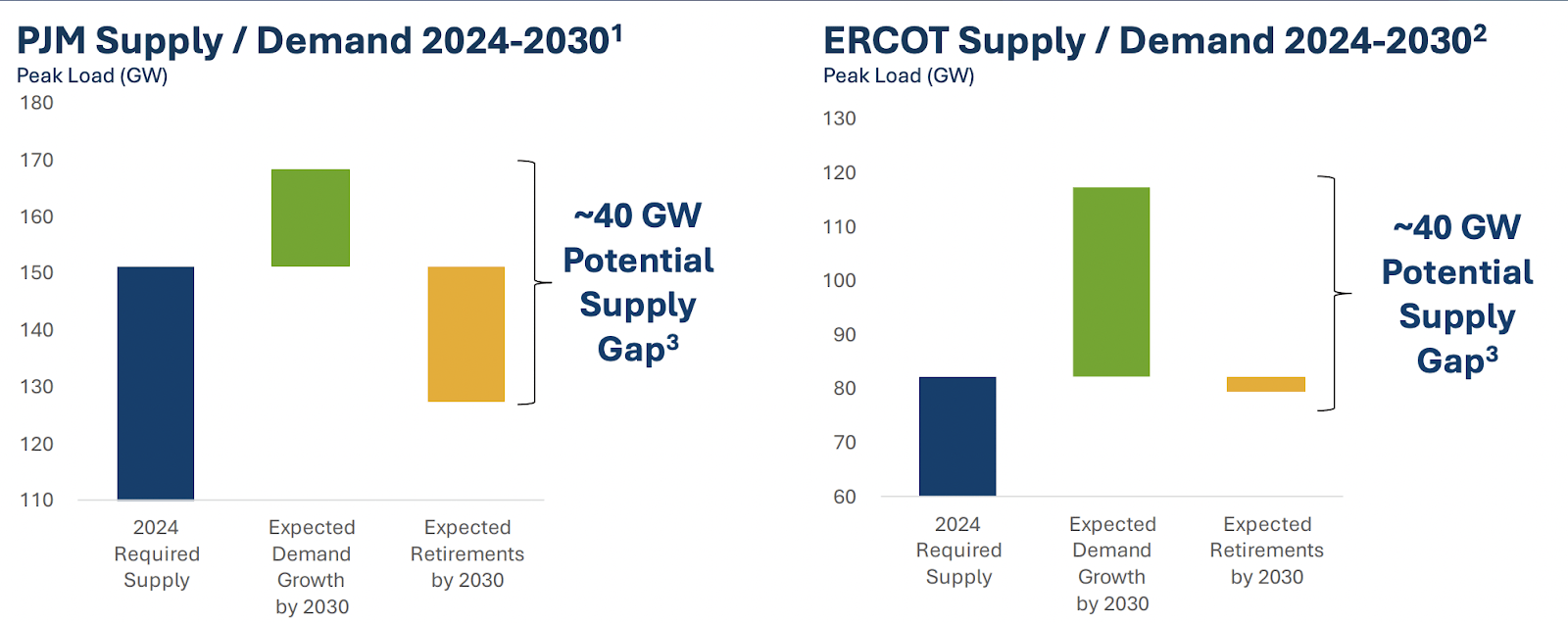

Energy Demand & Supply (Vistra)

In terms of the outlook, Burke emphasized:

Our integrated business model, which combines critical dispatchable generation assets with a premier retail business, positions us well to create long-term value in the current volatile and growing markets. Given our hedging activity over the past several months and the recent 2025-2026 PJM planning year auction results, we are raising our estimated 2025 ongoing operations adjusted EBITDA mid-point opportunity range by $200 million to $5.200 billion to $5.700 billion -Q2 Call.

CFO, Kris Moldovan, reinforced this outlook by discussing the company’s capital allocation strategy. She mentioned that despite the stock price increase, they still see their shares trading at an elevated free cash flow yield. Vistra’s valuation, combined with a robust share repurchase program—targeting at least $2.25 billion through this year and 2025, meaning there’s a lot of upward pressure on shares that’s coming up.

In March, the company invested in zero-carbon energy generation with the completion of their acquisition of Energy Harbor Corp, which expanded their nuclear power capabilities, adding approximately 4,000 megawatts of 24/7 nuclear generation capacity to their portfolio. This makes the company the second-largest competitive nuclear fleet operator in the U.S., while sustaining a cleaner energy future and maintaining grid reliability.

With these investments, the company is forecasted to experience strong, exponential growth over the next five years, as highlighted by recent analyst estimates. The company’s earnings per share (EPS) is expected to grow from $5.25 this year to $15.17 by 2028. Wow.

Analysts have also revised their estimates upwards multiple times over the last three months, reflecting an increasing confidence in Vistra’s growth. Revenue projections show a similar upward trend, with expected growth from $16.37 billion by year-end to $23.40 billion by 2028.

Growth May Appear Conservative

Texas operates the largest deregulated electricity market in the United States, which has been in place since 2002 when the state modified their energy regulatory strategy.

Texas’ change in regulatory measures means that ERCOT utilities like Vistra benefit from a distinctly unique market structure that allows them to sell electricity directly to Texas-based consumers without the normal oversight or restrictions typically found in regulated markets. Vistra has the flexibility to set competitive rates, innovate in their energy offerings, and capitalize on market demand fluctuations, especially as Texas continues to see rising electricity needs driven by AI data centers and other high-energy industries.

Operating in an unregulated market like Texas allows them to respond quickly to market dynamics, such as spikes in demand or changes in energy prices. An unregulated market means Vistra is offered the opportunity to maximize revenue during periods of high demand, particularly in extreme weather conditions when electricity prices can soar. In the absence of price caps, Vistra fully captures the benefits of price spikes, unlike in regulated markets where rates are often constrained by government policies. The summation of this is that higher demand from the grid results in exponentially higher earnings results. It’s hard to forecast this. Analysts often lean on the conservative side as a result.

On this same note, I would also like to emphasize that Vistra is currently tracked by only a small group of analysts, with estimates from just three or four of them guiding market expectations a few years out. When fewer analysts are covering a stock, the range of opinions and forecasts tends to be narrower, which in my experience has led to less aggressive price targets and earnings estimates.

With this, the Texas energy grid is also increasingly facing immense strain due to rising demand brought by the state’s booming population and energy-intensive sectors like data centers and AI technology. As Texas is the only state in the continental U.S. with its own electric grid, it operates in a deregulated environment where electricity prices are highly responsive to fluctuations in supply and demand.

As Texas continues to attract more businesses and residents, the consistent pressure on the grid suggests that demand—and therefore prices—will likely remain elevated, which Vistra can take advantage of to maximize their revenue.

Valuation

Vistra currently has strong EPS growth projections, with the latest consensus estimate for fiscal 2024 showing an 77.18% year-over-year increase to $5.25/share. Despite this impressive growth, Vistra’s shares are trading at a forward P/E ratio of just 15.51, notably below the sector median P/E of 16.92.

I find this valuation discrepancy to be surprising given the company’s tech-level growth rates. I think the market’s hesitation likely stems from concerns about the consistency and quality of Vistra’s earnings, as proven by their lower profitability metrics relative to the sector. For example, their gross profit margin stands at 34.68%, below the sector median of 45.34%.

Even with this, I think this perceived risk seems overblown, meaning Vistra is being underpriced. As Vistra continues to deliver on their growth projections, especially post integration of Energy Harbor, the consistency of earnings should improve.

If the company’s P/E ratio were to converge to the sector median of 16.90, this would represent a potential upside of roughly 9% not including the dividends paid or the effects of a buyback program on reducing share count, increasing EPS, and fighting to keep the P/E lower.

Risks

In my opinion, grid strain is good for earnings, but terrible if the grid completely fails. The Electric Reliability Council of Texas (ERCOT) has flagged the high probability of grid strain during periods of extreme weather, particularly during high heat or cold snaps.

If we saw a major grid failure, it would severely disrupt Vistra’s ability to operate and likely upend stability for the company as a whole. This strain on the grid is exacerbated by the state’s growing demand for electricity (as I mentioned before), which has seen record-breaking peaks as teetered on severe outages. A massive outage is almost surely a notable operating loss event. Think of it as a probability tail risk.

To counter this, Texas has added a huge capacity in renewable energy, with wind and solar adding a combined 31,000 megawatts to the grid during peak demand periods and lowering the probability of catastrophic failure. The state is witnessing a surge in wind and solar energy projects to bolster the state’s power supply, making it the top state for wind power and second in solar energy behind California.

While this article is on Vistra, a way to play the build out of wind and solar is a smaller company called Primoris (PRIM), which has capitalized on this trend, reporting a 25% surge in revenue from their energy segment, driven by solar and natural gas projects. As these renewable projects increase power supply, we’ll likely see the risk of grid failure drop. But this also increases the risk that energy prices in Texas may slightly decline due to the expanded capacity. It’s a unique trade-off, but one I think Vistra (and other utilities in Texas) are managing. By buying power generation facilities like the ones from Energy Harbor, they’re bringing on really durable supply. Having the best control of durable supply for a volatile grid gives you an edge. Vistra is doing this.

Bottom Line

Vistra delivered a strong quarter, but this article is more than just a commentary on the quarter: it’s me stating my belief that the company still has room to run. Despite promising numbers, shares continue to trade below the sector median, I really think this will not last forever. With the company’s earnings set to be far more consistent, durable, and higher in the future, this discrepancy presents a really compelling opportunity for investors.

Vistra’s energy generation assets remain critical in powering the AI data centers of tomorrow that require stable, 24/7 energy supply. Really, this positions the company as an essential player in meeting the growing demand from data centers, further supporting their market position as a utility company with tech like growth. Given this factors, I think shares are a strong buy. I am excited to see where the company goes from here.